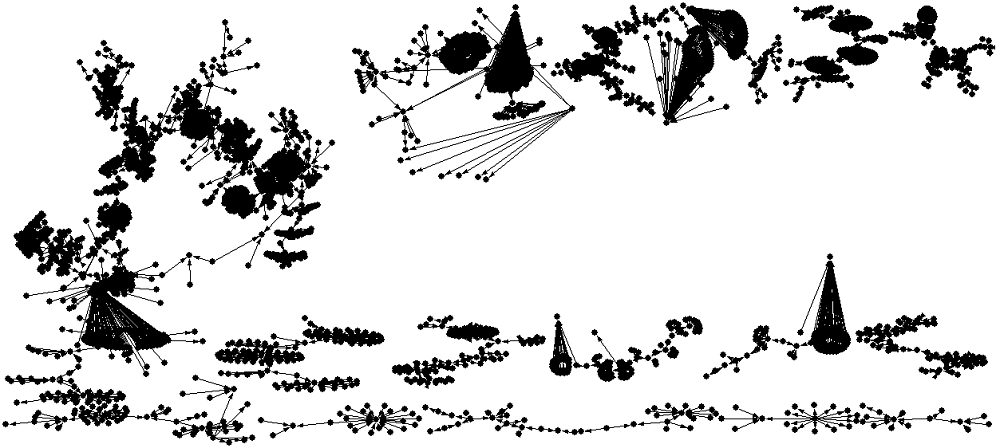

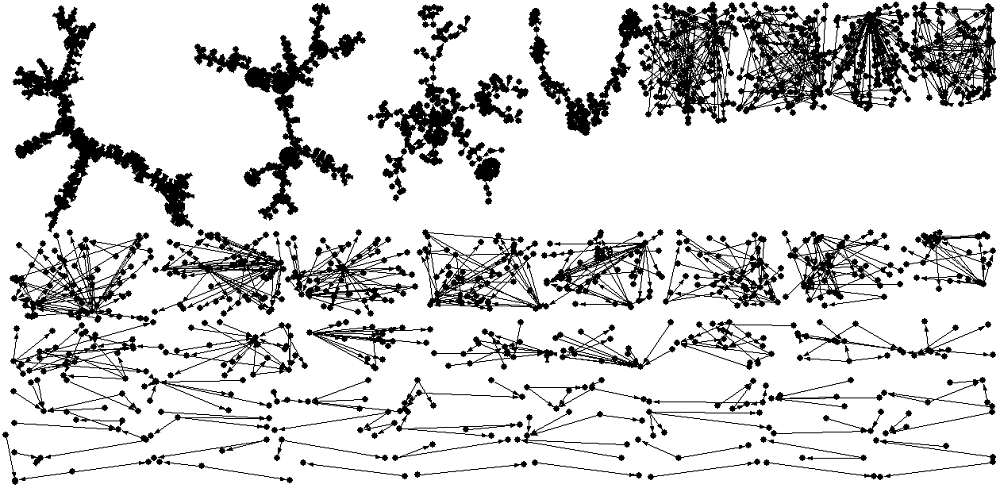

[Objective] This paper proposes a weighted network for stock intraday trading, and selects the main parameters for network features, aiming to identify the ultra-short-term market manipulations. [Methods] We constructed the weighted network for stock intraday trading with tick data, and used the order ID as nodes. The lines of network were the dealing orders, and the weights of line values were actual trading volumes. Analytical software Pajek5.03 and Ucinet6 were used to obtain the statistical parameters of complex networks for the proposed model. [Results] The nine network parameters, such as weighted average degree and network density, can be used as the main parameter to determine the stock manipulation. The overall accuracy values of our model with internal and external samples were 93.58% and 87.73%. [Limitations] We only retrieved the bull market data from 2015, while the bear market data were not collected. [Conclusions] This study helps authorities identify and crack down on the stock trading manipulation.

Ögüt H, Doganay M, Aktas R . Detecting Stock-price Manipulation in an Emerging Market: The Case of Turkey[J]. Expert Systems with Applications, 2009,36(9):11944-11949.

[2]

Diaz D, Theodoulidis B, Sampaio P . Analysis of Stock Market Manipulations Using Knowledge Discovery Techniques Applied to Intraday Trade Prices[J]. Expert Systems with Applications, 2011,38(10):12757-12771.

[3]

Comerton-Forde C, Putniņš T J . Measuring Closing Price Manipulation[J]. Journal of Financial Intermediation, 2011,20(2):135-158.

[4]

Adamic L, Brunetti C, Harris J H , et al. Trading Networks[J]. Econometrics Journal, 2017,20(3):S126-S149.

[5]

Maxim M R, Ashif A S M . A New Method of Measuring Stock Market Manipulation Through Structural Equation Modeling (SEM)[J]. Investment Management and Financial Innovations, 2017,14(3):54-61.

( Li Zhihui, Zhou Mi . Research on Measurement and Influencing Factors of Manipulation in China’s Stock Market: Based on the Characteristics of Listed Companies[J]. Journal of Central University of Finance & Economics, 2018(12):25-36.)

( Zhang Jianfeng, Fu Qiang, Du Jinzhu . Study on the Manipulation Anticipation of Listed Companies’ Stock Prices Based on Logistic Model[J]. Journal of Xi’an University of Technology, 2018,34(2):240-245.)

( Li Zhihui, Wang Jin, Li Mengyu . A Study on China’s Stock Market Manipulation’s Effects on Market Liquidity: Based on Closing Price Manipulation Behavior’s Identification and Monitoring[J]. Journal of Financial Research, 2018(2):135-152.)

[10]

Sun X, Cheng X, Shen H , et al. Distinguishing Manipulated Stocks via Trading Network Analysis[J]. Physica A: Statistical Mechanics and Its Applications, 2011,390(20):3427-3434.

[11]

Jiang Z, Xie W, Xiong X , et al. Trading Networks Abnormal Motifs and Stock Manipulation[J]. Quantitative Finance Letters, 2013,1(1):1-8.

[12]

Sun X, Shen H, Cheng X , et al. Detecting Anomalous Traders Using Multi-slice Network Analysis[J]. Physica A: Statistical Mechanics and Its Applications, 2017,473:1-9.

[13]

Shi F, Sun X, Shen H , et al. Detect Colluded Stock Manipulation via Clique in Trading Network[J]. Physica A: Statistical Mechanics and Its Applications, 2019,513:565-571.

[14]

Ding C, Yao H, Du J , et al. Cascading Failure in Interconnected Weighted Networks Based on the State of Link[J]. International Journal of Modern Physics C, 2017,28(3):1750040.