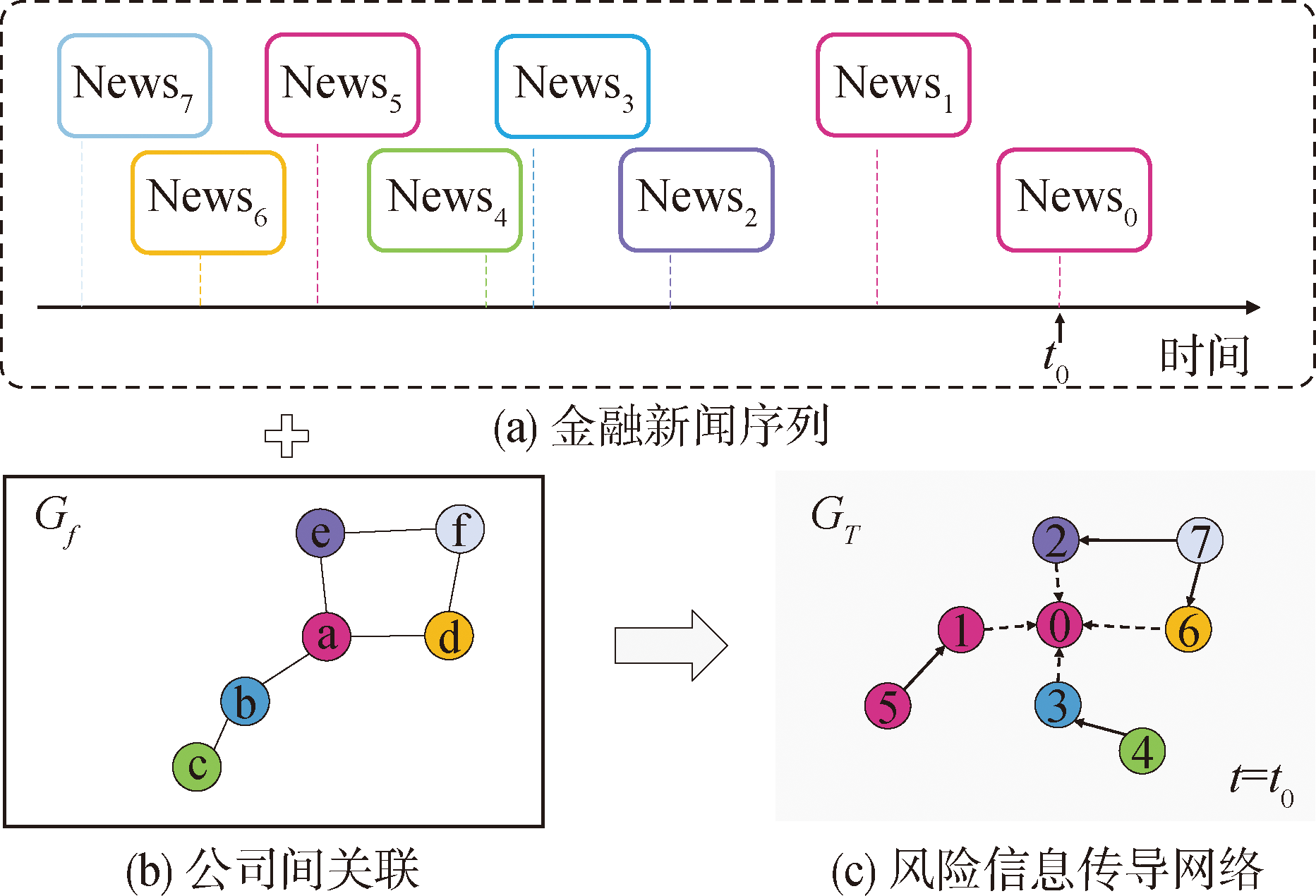

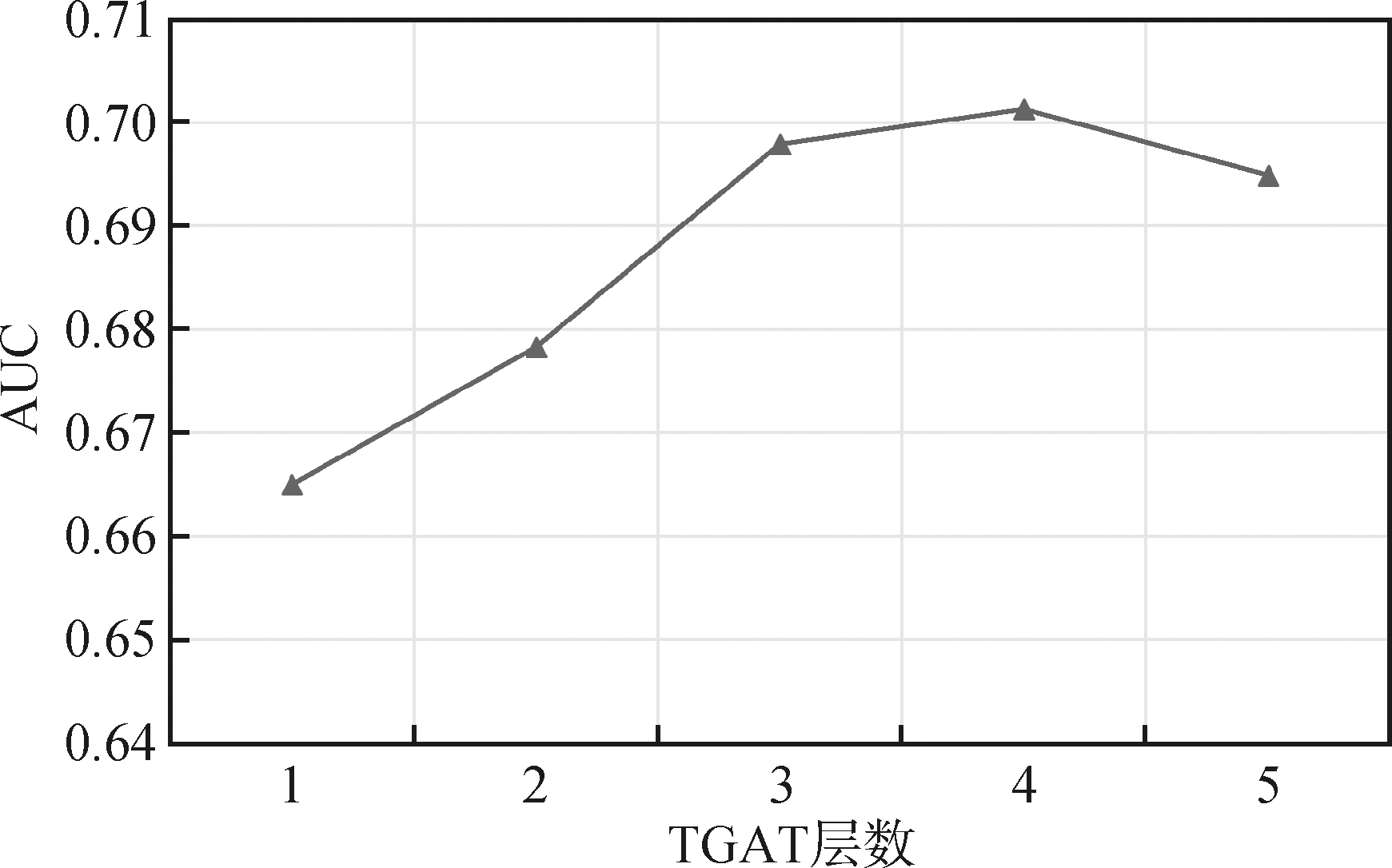

[Objective] This paper studies financial news representations and the supply chain characteristics of particular companies. Then it utilizes these representations and inter-company associations to improve the prediction of public opinion risks for the target company. [Methods] Firstly, we embedded the company association knowledge into financial news texts based on attention mechanism and Bi-LSTM to learn financial news representation to a specific company. Secondly, we organized the financial news sequence into a news risk transmission network based on inter-company knowledge association. Finally, we used the TGAT layer to model the temporal transmission patterns of risk information through inter-company association and aggregate the risk information to predict the financial public opinion risk of the target company. [Results] The proposed method achieved an accuracy of 0.6246 and an AUC of 0.7021 in the financial public opinion risk prediction task, outperforming the baseline methods. [Limitations] The new model only uses the statistical knowledge associations between stocks of the listed companies and does not incorporate other types of inter-company knowledge associations. [Conclusions] The proposed model can effectively learn risk information relevant to the target company from financial news and the temporal transmission characteristics of public opinion risk in inter-company associations. It demonstrates good financial risk prediction performance.

陈昊冉, 洪亮. 融合知识关联与时序传导的金融舆情风险预测模型*[J]. 数据分析与知识发现, 2023, 7(11): 1-13.

Chen Haoran, Hong Liang. Financial Public Opinion Risk Prediction Model Integrating Knowledge Association and Temporal Transmission. Data Analysis and Knowledge Discovery, 2023, 7(11): 1-13.

Hisano R, Sornette D, Mizuno T, et al. High Quality Topic Extraction from Business News Explains Abnormal Financial Market Volatility[J]. PLoS ONE, 2013, 8(6): e64846.

doi: 10.1371/journal.pone.0064846

[2]

Atkins A, Niranjan M, Gerding E. Financial News Predicts Stock Market Volatility Better Than Close Price[J]. The Journal of Finance and Data Science, 2018, 4(2): 120-137.

doi: 10.1016/j.jfds.2018.02.002

[3]

Chang C Y, Zhang Y, Teng Z, et al. Measuring the Information Content of Financial News[C]// Proceedings of the 26th International Conference on Computational Linguistics:Technical Papers. 2016: 3216-3225.

[4]

Loughran T, McDonald B. When is a Liability Not a Liability? Textual Analysis, Dictionaries, and 10-Ks[J]. The Journal of Finance, 2011, 66(1): 35-65.

doi: 10.1111/jofi.2011.66.issue-1

[5]

Wang C J, Tsai M F, Liu T, et al. Financial Sentiment Analysis for Risk Prediction[C]// Proceedings of the 6th International Joint Conference on Natural Language Processing. 2013: 802-808.

[6]

Tsai M F, Wang C J. Financial Keyword Expansion via Continuous Word Vector Representations[C]// Proceedings of the 2014 Conference on Empirical Methods in Natural Language Processing. 2014: 1453-1458.

(Jiang Fuwei, Meng Lingchao, Tang Guohao. Media Textual Sentiment and Chinese Stock Return Predictability[J]. China Economic Quarterly, 2021, 21(4): 1323-1344.)

[8]

So M K P, Mak A S W, Chu A M Y. Assessing Systemic Risk in Financial Markets Using Dynamic Topic Networks[J]. Scientific Reports, 2022, 12(1): Article No. 2668.

[9]

Cheng D, Yang F, Wang X, et al. Knowledge Graph-based Event Embedding Framework for Financial Quantitative Investments[C]// Proceedings of the 43rd International ACM SIGIR Conference on Research and Development in Information Retrieval. 2020: 2221-2230.

[10]

Duan J, Zhang Y, Ding X, et al. Learning Target-Specific Representations of Financial News Documents for Cumulative Abnormal Return Prediction[C]// Proceedings of the 27th International Conference on Computational Linguistics. 2018: 2823-2833.

[11]

Hu Z, Liu W, Bian J, et al. Listening to Chaotic Whispers: A Deep Learning Framework for News-oriented Stock Trend Prediction[C]// Proceedings of the 11th ACM International Conference on Web Search and Data Mining. 2018: 261-269.

[12]

Ding X, Shi J, Duan J, et al. Quantifying the Effects of Long-term News on Stock Markets on the Basis of the Multikernel Hawkes Process[J]. Science China Information Sciences, 2021, 64(9): 192102.

doi: 10.1007/s11432-020-3064-4

[13]

Xu W, Liu W, Xu C, et al. REST: Relational Event-driven Stock Trend Forecasting[C]// Proceedings of the Web Conference 2021. 2021: 1-10.

(Hong Liang, Ma Feicheng. Knowledge Association Analysis and Big Knowledge Graph Construction for Big Data Management and Decision-making[J]. Journal of Management World, 2022, 38(1):207-219.)

(Liu Zhenghao, Qian Yuxing, Yi Tianlong, et al. Constructing Knowledge Graph for Financial Securities and Discovering Related Stocks with Knowledge Association[J]. Data Analysis and Knowledge Discovery, 2022, 6(2/3):184-201.)

[16]

Liang Z, Pan D, Deng Y. Research on the Knowledge Association Reasoning of Financial Reports Based on a Graph Network[J]. Sustainability, 2020, 12(7): 2795.

doi: 10.3390/su12072795

(Hong Liang, Ouyang Xiaofeng. Knowledge Association Discovery and Risk Analysis Based on Financial Equity Knowledge Graph[J]. Journal of Management Sciences in China, 2022, 25(4): 44-66.)

(Tang Xuli, Ma Feicheng, Fu Weigang, et al. Research on Financial Knowledge Representation and Risk Identification from Knowledge Connection Perspective[J]. Journal of the China Society for Scientific and Technical Information, 2019, 38(3):286-298.)

[19]

Theil C K, Broscheit S, Stuchenschmidt H. PRoFET: Predicting the Risk of Firms from Event Transcripts[C]// Proceedings of the 28th International Joint Conference on Artificial Intelligence. 2020: 5211-5217.

[20]

Tsai M F, Wang C J. On the Risk Prediction and Analysis of Soft Information in Finance Reports[J]. European Journal of Operational Research, 2017, 257(1): 243-250.

doi: 10.1016/j.ejor.2016.06.069

[21]

Lin T W, Sun R Y, Chang H L, et al. XRR: Explainable Risk Ranking for Financial Reports[C]// Proceedings of Joint European Conference on Machine Learning and Knowledge Discovery in Databases. Springer, Cham, 2021: 253-268.

[22]

MacKinlay A C. Event Studies in Economics and Finance[J]. Journal of Economic Literature, 1997, 35(1): 13-39.

[23]

Kothari S P, Warner J B. Econometrics of Event Studies[A]//Handbook of Empirical Corporate Finance[M]. Elsevier, 2007: 3-36.

[24]

Devlin J, Chang M W, Lee K, et al. BERT: Pre-Training of Deep Bidirectional Transformers for Language Understanding[OL]. arXiv Preprint, arXiv:1810.04805.

[25]

Huang A H, Wang H, Yang Y. FinBERT: A Large Language Model for Extracting Information from Financial Text[J]. Contemporary Accounting Research, 2022. https://doi.org/10.1111/1911-3846.12832.

(Mao Ruibin, Zhu Jing, Li Aiwen, et al. Construction of Knowledge Graph of Industry Chain Based on Natural Language Processing[J]. Journal of the China Society for Scientific and Technical Information, 2022, 41(3):287-299.)

[27]

Wang Z, Zhang J, Feng J, et al. Knowledge Graph Embedding by Translating on Hyperplanes[C]// Proceedings of the AAAI Conference on Artificial Intelligence. 2014: 1112-1119.

[28]

Xu D, Ruan C, Korgeoglu E, et al. Inductive Representation Learning on Temporal Graphs[C]// Proceedings of International Conference on Learning Representations. 2020.

[29]

Kipf T N, Welling M. Semi-supervised Classification with Graph Convolutional Networks[C]// Proceedings of International Conference on Learning Representations. 2017.

[30]

Hamilton W L, Ying Z, Leskovec J. Inductive Representation Learning on Large Graphs[C]// Proceedings of the 31st International Conference on Neural Information Processing Systems(NeurIPS). 2017: 1025-1035.

[31]

Yun S, Jeong M, Kim R, et al. Graph Transformer Networks[C]// Proceedings of the 33rd International Conference on Neural Information Processing Systems (NeurIPS). 2019: 11983-11993.