王伟 , KevinZhu

, KevinZhu

Wang Wei, Kevin Zhu

中图分类号: TN948.61 G35

通讯作者:

收稿日期: 2018-02-1

修回日期: 2018-04-11

网络出版日期: 2018-07-25

版权声明: 2018 《数据分析与知识发现》编辑部 《数据分析与知识发现》编辑部

基金资助:

展开

摘要

【目的】基于Web的众筹模式成为新的融资渠道, 倍受政府和投资者的关注, 但是众筹研究并不广泛。本文针对众筹模式的现状, 探讨众筹模式结构性、趋势性的研究进展。【文献范围】从 Web of Science、CNKI等数据库中分别以“众筹(Crowdfunding, Crowdfinancing, Crowdinvesting)”、“P2P借贷(P2P Lending)”等检索词检索获得中英文相关文献101篇。【方法】通过文献计量学和数据分析方法, 针对众筹相关概念及内涵、模式差异、影响因素与发展趋势进行系统的文献提炼与评析, 分面从众筹平台、项目描述、社会关系、地理位置以及项目质量等方面分析影响众筹项目成功率的因素。【结果】众筹项目融资受多方面因素影响, 尤其不能忽视非质量因素, 项目融资者与投资者呈现显著的行为模式的差异, 投融双方的行为共同决定众筹项目的前景。【局限】众筹模式的研究还并不深入。【结论】众筹模式具有较大的可探索空间, 未来需要结合其他领域的研究对众筹模式进行更加深入的研究, 例如: 心理学、行为学、金融学等。

关键词:

Abstract

[Objective] The web-based crowdfunding has become a new channel for fund-raising, which got more and more attention from governments and investors. However, limited research has been conducted on crowdfunding. This paper reviews the latest studies on crowdfunding, and discusses its trends. [Coverage] We retrieved 157 Chinese and English papers from Web of Science and CNKI using the keywords of “Crowdfunding”, “Crowdfinancing”, “Crowdinvesting” or “P2P Lending”. [Methods] By literature metrology and data analysis methods, we introduce the definitions and classifications of crowdfunding. Then we study the factors which influence the successful campaigns from the following aspects: platform of crowdfunding, description of the projects, social relationship of the founders, geographical factors, as well as the quality signals of the projects. [Results] Results of the crowdfunding campaigns were influenced by many factors, especially the non-quality ones. There was significant difference between the investors and peoples seeking funding, which determined the prospect of each campaign. [Limitations] More research is needed to investigate the crowdfunding models [Conclusions] There are still much to be explored in crowdfunding models, such as from the psychology, behavioral science and finance perspectives.

Keywords:

对创业者而言, 创业初期最棘手的问题之一是融资[1]。市场调查表明, 2011年众筹市场规模为15亿美元; 2012年上升到27亿美元, 支持了100万个项目[2]; 2013年上升到61亿美元; 2014年更是迎来了爆发性增长, 达到162亿美元, 增幅达到167%; 2015年超过340亿美元; 2016年达到500亿美元, 增长迅猛[3]。在产品正式上市前, 众筹可以找到潜在客户, 这不但为初创企业提供了资金来源, 而且还提供了未来潜在消费群体, 使正在开发中的品牌和产品可以享受早期资金支持。而对于消费者来说, 可以在产品或品牌启 动期内从较低的价格中获益, 有助于初创企业推广产品[4], 众筹模式的经济意义重大。

众筹译自Crowdfunding、Crowdfinancing以及Crowdinvesting, 源于众包(Crowdsourcing)。众筹最朴素的定义是向大众筹集资金[5], 这一定义指出众筹的本质为大众参与。众筹是从数量众多的投资者中融资, 每个投资者只投入少量资金, 以支持融资者的活 动[2,6]。当众筹的环境被限制后, 其定义为:通过公开方式(如Internet), 以一定回报或者无偿捐赠的形式, 以一定资金来支持融资者的活动[2]。众筹还被定义为:融资者向无数人请求并获得资金或其他资源以支持某个项目发展的过程, 并向投资者提供金钱或非金钱回报的行为过程[2]。这一定义强调众筹不只是筹资, 还包括后期的项目实施与回报。还有定义为:融资者以公开的方式, 向公众筹集资金, 公众以无偿捐赠或者以收取回报的方式支持项目[7]。

众筹这种融资方式由来已久, 延伸到各个领域, 并改变了很多行业的游戏规则[8,9], 因此, 引起了政府的广泛关注[10], 但是对众筹模式的研究和应用还存在诸多不足。研究众筹模式、动态趋势, 识别互联网金融的发展轨迹, 对于洞察未来机会、规划研究活动、推动互联网金融创新、引导在线金融模式的发展具有重要的理论价值与实践意义。因此, 本文从众筹的定义、模式、影响因素、行为模式、法律监管等方面, 对已有研究进行梳理和评述。

文献之间的引用关系是定量刻画科学结构、揭示研究现状的文献计量方法。本研究的英文数据样本来源为汤森路透(Thomson Reuters)的Web of Science数据库。以“Title=(Crowdfunding, Crowd funding, Crowdfinancing, Crowdinvesting, P2P Lending, Micro-financing)、Databases=(SCI-EXPANDED, SSCI, CPCI-S, CPCI-SSH, CCR-EXPANDED, IC)、Document Types=(ARTICLE OR REVIEW)、Languages=(ENGLISH)、Timespan= 2008-2018”为检索条件, 所得922条文献题录中共有 4 893条引文来自SCI数据库。

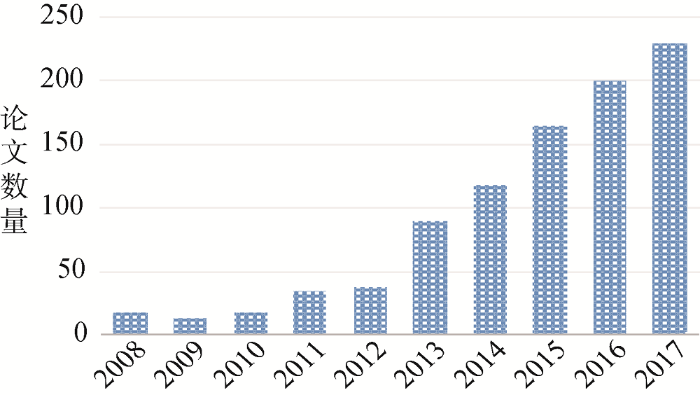

图1和图2分别展示了每年出版的文献统计和频繁关键词词云, 可以看到众筹有关的研究是从2013年才开始真正兴起的, 2013年以后每年均有100篇以上的文献被SCI数据库收录。而如果以论文的关键词进行分析, 已有文献较多集中在融资、政策、风险、借贷、股权等方面。

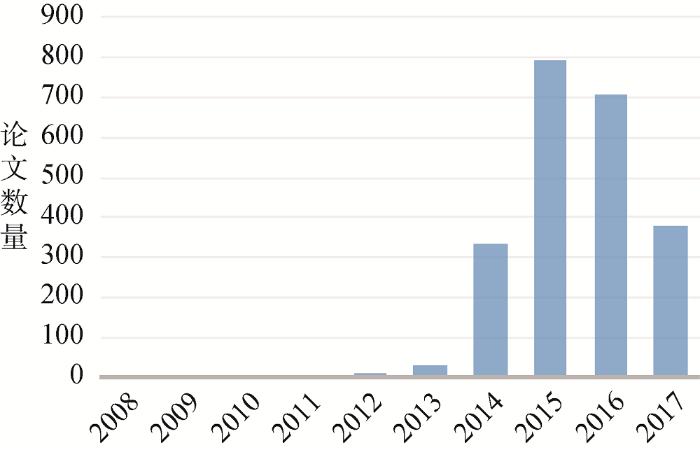

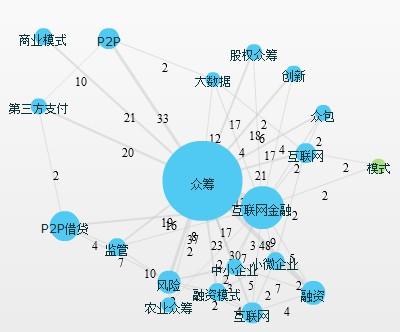

对于中文文献, 选择CNKI数据库作为文献的来源, 采用“众筹”、“众投”, “P2P借贷”等作为关键词进行检索, 一共得到2 251条中文检索结果, 如图3和图4所示。中文领域有关众筹的研究起步较晚, 直到2013年论文数量才超过10篇, 显然, 在中文领域的研究是从2014年才大规模展开的, 比国外研究稍晚, 而研究主题主要集中在互联网金融、P2P借贷和融资模式等。尤其值得一提的是国内关于农业众筹的研究比国外广泛得多, 这可能是由于中国是农业大国这一客观因素导致的。

综合英文和中文论文, 从中选取开创性、高引用的101篇代表性文献为对象, 用于分析众筹的融资模式、影响因素和行为模式。

根据融资目的以及回报方式的不同, 众筹模式分为:基于回报的众筹、基于股权的众筹、基于借贷关系的众筹、基于无偿捐赠的众筹等。Danmayr曾对91个众筹网站的模式进行调查统计, 结果如表1所示[11]。可以看出, 绝大多数众筹模式都是基于回报的。其次, 基于无偿捐赠的众筹也占据较大比例, 这得益于具有线下基础的公益活动逐步过渡到线上。

表1 各种众筹模式所占比例[

| 众筹模式 | 数量 | 比例 |

|---|---|---|

| 基于回报的众筹 | 34 | 37.36% |

| 基于无偿捐赠的众筹 | 26 | 28.57% |

| 基于股权的众筹 | 13 | 14.29% |

| 基于借贷关系的众筹 | 6 | 6.59% |

| 回报+捐赠模式 | 5 | 5.49% |

| 股权回报模式 | 3 | 3.30% |

| 借贷+回报模式 | 2 | 2.20% |

| 捐赠+借贷模式 | 1 | 1.10% |

| 借贷+股权+回报 | 1 | 1.10% |

| 合计 | 91 | 100.00% |

基于回报的众筹模式发展最快[7], 并诞生了全球最大的众筹平台 Kickstarter[12]。基于回报的众筹模式分为:

(1) 以Kickstarter为代表的“All-or-Nothing”模式;

(2) 以RocketHub为代表的“Keep-what-you-raise” 模式;

(3) 以Indiegogo为代表的混合模式。

All-or-Nothing指只有当筹资金额达到或超过预设的筹资目标才算成功, 融资者才能拿到筹集的资金; 而Keep-what-you-raise是指即使筹资金额没有达到预设目标, 融资者也可以支配已筹得的资金。表2给出三种模式的代表网站以及典型区别。

表2 基于回报的众筹项目三种模式的比较

| 筹资模式 | 代表网站 | 平台收费 | 慈善 项目 | 匿名 投资 | 多人 维护 | Alex 排名① | 融资者 限制 | 项目 分类 | 筹资 时间 | 项目成功率 |

|---|---|---|---|---|---|---|---|---|---|---|

| All-or-Nothing | Kickstarter.com | 未达到筹资目标则退款; 达到筹资目标收取8%-10%。 | 不支持 | 不支持 | 不支持 | 657 | 由于税收问题, 仅限美国公民 | 13 | 1~60天 | 约36%② |

| Keep-what-you-raise | RocketHub.com | 达到筹资目标收取4%; 未达到筹资目标收取8%。 | 支持, 但不推荐 | 不支持 | 支持 | 319074 | 无限制 | 4大类, 32小类 | 15~90天 | 未公布 |

| 混合模式(由融资者决定) | Indiegogo.com | 达到筹资目标收取4%; 未达到筹资目标收取9%。 | 支持 | 支持 | 支持 | 2178 | 无限制 | 24 | 1~60天 | -- |

②https://www.kickstarter.com/help/stats.

投资者的决策受项目质量的影响, 同时也受融资者社会关系的影响[13,14]。现有研究集中在项目质量的甄别、融资者的个人能力、以及社会关系准则在众筹平台的作用[15]。表3归纳了基于回报的众筹模式的影响因素。

表3 基于回报的众筹模式的影响因素

| 正相关 | 负相关 | |

|---|---|---|

| 发起方因素 | 融资者的准备充分度[13]; 口碑效应[16]; 融资者的性别[17]; 项目 更新[13,18]; 承诺的回报激励机制[19] | 由于顾及知识产权, 不能在项目描述中详细介绍项目[20]; 定价策略的错误使用[21] |

| 投资方因素 | 投资者之前受到融资者的支持, 或者建立了某种关系[22]; 集群效应[23] | 担心融资者滥用资金[20]; 担心项目不能履行承诺的回报[20] |

基于回报的众筹模式研究集中在融资者、投资者以及捐赠者的动机上[15]。部分投资者并不在意项目的回报, 他们更关心投资能否带来心理上的好感。这部分投资者通常是融资者的亲朋好友[24], 道德因素也具有重要作用[25]。项目对外传递的质量信息会影响融资成功率, 这包括准备充分度、描述方式、其他投资者的态度、融资者的个人特质、信用以及社会关系等[26]。

无偿捐赠的众筹模式是传统的慈善活动向互联网延伸的一种方式, 对投资者没有任何股权或者物质上的回馈, 志愿者是由于自身的利他心理而支援融资者, 基于无偿捐赠的众筹研究还没有广泛展开, 大多数集中在支持者捐赠的动机上。表4归纳了无偿捐赠众筹模式的影响因素。

表4 基于无偿捐赠的众筹模式的影响因素

| 影响方 | 影响因素 | 影响方向 |

|---|---|---|

| 筹资方 | 慈善机构展示出来的效率[27] | 正相关 |

| 筹资方 | 慈善机构所在领域的竞争情况[27] | 负相关 |

| 筹资方 | 筹集资金的目标越高, 越会阻碍投资者 投资兴趣[27] | 负相关 |

| 筹资方 | 社会化网络资源的使用[28] | 正相关 |

| 筹资 项目 | 有明确筹资目标的项目筹得的资金是其他项目的两倍以上, 并且更容易吸引融资者的关注和未来再次投资[29] | 正相关 |

| 投资方 | 其他人的投资决策[30] | 正相关 |

无偿捐赠众筹项目一旦成功, 通常能够筹集到高于预设目标的资金, 但投资人数较少。这表明, 愿意支持慈善项目的人占少数, 但是投资金额却很大[31]。

融资者承诺投资者, 如果创业成功, 将以一定的股权作为回报。由于股权众筹项目的特殊性, 在项目运作之前, 投资者很难全面了解项目, 因此, 投资者对项目的评价常常受到其他投资者行为的影响[32]。

项目启动之前, 融资者会咨询亲朋好友, 他们也因此会成为项目早期的投资者。如果早期投资者不是这一类人, 则表明项目的质量以及创始人的能力已经获得广泛的认可, 这对其他支持者的投资决策具有激励作用[33]。对于股权众筹模式, 融资成功与否受诸多因素的影响, 但是性别的影响尤其重要[34]。这一方面是由于女性管理的企业比例小, 另一方面是由于女性对外部融资的认知所致[35]。

文献[7]总结了产品预售和股权众筹各自的适应 条件:

(1) 相对市场容量而言, 如果启动资金较少, 企业更倾向于采用预先出售的模式;

(2) 其他情况下, 股权众筹模式更加适合。

基于借贷关系的众筹模式是银行金融的延伸, 受到诸多因素影响[36,37,38,39]。其中, 文化差异对借贷关系的影响巨大。筹资方与投资方1个标准差的文化差异会导致至少30次以上投资行为的减少; 而1个标准差的地理位置差异只会减少0.23次投资行为。但是, 文化差异和地理位置有一定的替代效应, 即地理距离每增加50%会导致文化差异的影响降低30%[40]。

信息不对称是阻碍投资的因素之一[41], 早期的借款者对市场风险并不完全了解, 但随着时间的推移, 学习成为减弱风险的有效方法, 市场会倾向于排除 次级债借贷者, 即传统的线下信用市场逐渐向线上 转移[42]。

科研众筹是针对科研人员的众筹模式, 科研众筹除了筹集资金外, 还为公共宣传、科学教育和科学普及提供了机会。以中国科研现状来说, 传统的科研经费筹集渠道往往存在经费不足、行政化色彩过强、学术自主性不够等方面的缺陷, 这在一定程度上制约了学术研究的发展[43], 众筹一定程度上解决了这个问题。科研众筹投资者之间存在模仿行为[44], 融资者的社会关系是科研众筹项目成功的主要影响因素。那些花时间培育关系的科学家, 可能会获得超越金钱收益的回报。科研众筹鼓励科学研究过程的透明度和公 众参与, 培养科学家和非科学家之间的长期合作关系[45]。

另一方面, 科研机构作为众筹平台参与融资是一个值得探讨的话题。现有的基于Web的平台只是融资者和投资者的中介, 本身不对项目质量做任何评估。事实上, 面对来自不同领域的项目, 众筹平台也难以评估每个项目的质量。而大学作为研究型机构, 有能力对项目质量进行专业性评估。因此, 大学作为沟通投资人和企业的中间桥梁更加合适[46]。

公众科学项目的组织方式有别于传统的科学组织方式, 开放参与的特点区别于其他科学创新制度。尽管公众科学项目解决了一些实际问题, 但是对于资助机构和决策者却提出了新的挑战[47]。

公众科学众筹模式有三个显著特点:

(1) 公众科学不只是资金支持, 还包括数据共享、设备共享、计算能力分享等[48];

(2) 公众科学参与者众多, 对参与者身份没有明确的限制, 只要能够提供资源即可。而传统科学项目中, 科研人员倾向于双向选择合作者[47];

(3) 公众科学的成果共享, 以Galaxy Zoo项目为例, 全部公开由志愿者分类的数据[49]。

由于公众科学通常有当地的大众参与, 因此, 未来的一个发展方向是使用当地的参与者资源, 解决区域性问题或者不同区域之间的比较研究[50]。

选择合适的众筹平台对成功融资至关重要[51]。同时, 众筹平台对项目的排序以及推荐也会影响融资。互联网信息过于丰富, 用户面临信息过载, 投资者更倾向那些容易找到的项目, 因此, 排序靠前的项目更容易获得融资。Web平台对项目的推荐会显著影响融资成功率[52]。众筹平台会提示最新项目和即将结束的项目, 这在一定程度上造成项目新上架或即将结束的一段时期是投资的高峰期[13]。

项目描述信息是投资者了解项目的途径, 也是促成融资成功的重要因素, 因此描述信息的吸引力是融资者需要关注的问题[13]。有学者通过文本分析揭示了文本长度和可读性与融资结果的关系,文本描述中使用特定的词汇有助于融资成功[53]。在相同条件下, 项目描述越容易理解(包括易读性等多项指标), 越是表明融资者受过更好的教育、拥有更稳定的收入以及更高的社会地位[54], 这样的融资者更值得信任[55]。表5归纳了项目描述因素对众筹项目成功融资的影响。

表5 项目描述因素对众筹项目成功融资的影响

| 分类 | 影响因素 | 影响方向 |

|---|---|---|

| 多媒体因素 | 提供项目视频介绍[56] | 正相关 |

| 视频制作水平[13] | 正相关 | |

| 文本描述因素 | 描述文本的可读性[57] | 正相关 |

| 负面文本情感信息[57] | 负相关 | |

| 主观性的描述[58] | 负相关 | |

| 文本描述中存在潜在的欺诈性线索[59] | 负相关 | |

| 修辞学策略的使用[60] | 正相关 | |

| 众筹模式需要在线描述项目创意, 这对所有访客都是公开的, 因此存在创意被窃取的威胁, 市场上可能涌现相似的产品[61], 因而项目描述不够具体 | 负相关 | |

| 回报描述因素 | 回报等级设置缺乏区分度[62] | 负相关 |

项目推介渠道不畅是众筹失败的原因之一, 将融资者的社会关系应用于众筹项目的社会化推荐有助于融资成功率的提高[63], 但这种方法理论上有效, 实践中却难以操作。社会关系来自两个方面, 分别是融资者的社会关系和投资者的社会关系[23]。用户行为具有集群效应, 这种集群行为实际上是个人在项目质量不确定条件下, 降低风险的理性行为[64]。表6分别从融资者和投资者角度归纳了社会关系因素对众筹项目成功融资的影响。

表6 社会关系因素对众筹项目成功融资的影响

| 社会关系 | 正相关 | 负相关 |

|---|---|---|

| 发起方 | 社会化推荐[63];社会化网络上的好友数量(例如: Facebook)[13];投资者与融资者的互动[65] | 融资者不能吸引来自亲朋好友的资金支持[24,66];个人融资者比团队融资者更难融资成功[67] |

| 投资方 | 集群行为[24,37,40,64];知名投资者参与或者大客户参与[67] | 早期投资行为不足[68,69];投资者与投资者, 投资者与融资者缺乏交流[62] |

投资者和融资者双方的距离不容忽视[70]。虽然投资者无论身处何处均可以参与投资, 但大多数早期的投资者来自距离融资者较近的地方。显然地理位置接近有利于收集项目及融资者的信息, 也便于监控项目进度以及提供必要的支持。尽管已经普遍证实了距离因素会影响投资者的投资行为, 但是这种位置效应同时受到项目的性质和投资者类型的影响[71]。表7归纳了地理位置因素对众筹项目成功融资的影响。

表7 地理位置因素对众筹项目成功融资的影响

| 影响因素 | 影响方向 |

|---|---|

| 约31%的早期投资来自朋友和家人[72], 这些人对融资者的品行和专业能力有较客观的评价[66], 因此投资者地理位置较近是对项目质量的肯定。 | 正相关 |

| 对于线下的风险投资, 投融资双方的平均距离仅为70英里; 而50%的天使投资与目标企业的距离也在半天行程范围内[73], 投资者偏好距离较近的项目。 | 正相关 |

| 早期投资行为是对项目质量的肯定, 对其他投资者(地理位置较远)具有激励作用[74]。 | 正相关 |

| 地理位置因素导致了对Web众筹平台不同的信息使用模式, 非亲朋好友更倾向于使用搜索引擎检索项目, 或依赖众筹平台的推荐功能。朋友和家人则不然, 他们不受信息检索的驱动, 这种行为模式在首次投资时尤为明显[24]。 | 正相关 |

| 由于项目性质的差异, 投资者对不同项目类别的地理位置效应(本地偏好)存在显著差异, 例如投资者通常喜欢地理位置较近的食品类项目, 而科技类项目则不受此影响[75]。 | 依项目性质而定 |

对美国50家风投企业的调查发现, 创始人经过一段时间会离职, 而公司的核心业务则长期不变[76]。这表明项目质量对企业发展或许比创始人或管理团队更重要, 但相反观点也很普遍。例如, 受过高等教育的创业者, 往往能够创造更加务实的商业计划[77]。对此争议, 研究者持不同观点, 一方认为创业者的创意以及市场空间更重要[78]; 而另一方认为创业者的个人特质、能力、激情更重要[79]。表8归纳了项目质量因素对众筹项目成功融资的影响。

表8 项目质量因素对众筹项目成功融资的影响

| 归类 | 影响因素 | 影响方向 |

|---|---|---|

| 项目内容方面的 质量展示 | 筹资目标高的项目不易获得投资者的认可, 而低目标更易成功[13], 融资失败项目的筹资目标是成功项目的5倍以上[15]。 | 负相关 |

| 专利权(或者知识产权)的申明[80]。 | 正相关 | |

| 由于担心创意被窃取, 而不能在项目描述中详细描述项目的内容[81]。 | 负相关 | |

| 融资人方面的 质量展示 | 好项目通常以高质量的视频为卖点, 融资者对自身信息的披露(如所在城市、职业、学历)也能显示项目质量[13]。 | 正相关 |

| 在激烈竞争的环境下, 管理经验有助于提升企业对人力资本以及社会资本的吸收能力[82]。 | 正相关 | |

| 乐观的融资者对于成功充满信心, 有激情的融资者更容易获得成功[45]。 | 正相关 |

经验丰富的融资者在筹资技巧、沟通、社会关系上优于首次融资者, 会更容易获得成功[37]。

融资者针对项目的进展发布更新信息, 更新频率和更新模式会显著影响筹资的成功率。针对Kickstarter的研究发现, 没有更新信息的项目融资成功率仅为32.6%, 而提供更新的成功率为58.7%。在所有更新主题中, 最有效的是提醒, 其次是项目进度的汇报, 对成功率影响最小的是疑问解答[18]。

投资者参与众筹的动机有: 获得回报[16]; 加入社交圈[83]; 出于乐趣[84]。筹资期内, 投资行为会呈现U型规律[15], 截至效应广泛存在, 约2/3项目筹资成功都是在最后一周完成的[15]。

投资者存在集群效应[85], 如果用户集群不理性, 集群会自我加强而淘汰一些非理性用户; 如果是理性的, 用户会对已有的集群进行甄别[37]。

由于各种原因, 投资者在一段时间后对社区的贡献会逐渐下降(Time Effects)[86]。另一种行为模式是投资者更喜欢在周中而不是在周末进行投资。通常, 从周日开始逐渐增加, 周四到达顶峰, 然后开始下降, 周六到达谷底[15]。而在投资者选择项目上, 群体智慧对众筹具有正面影响[87,88]。更重要的, 投资者对不同项目类别存在不同的判断标准, 例如科技类项目通常关注项目创意, 而艺术类项目关键在于融资者的个人特质及其艺术成就[89]。

美国于2012年颁布JOBS法案, 该法案主要针对股权众筹模式, 它以法律形式承认了股权众筹的合法性, 并试图将众筹的管理成本降到最低[90]。尽管如此, 市场上仍然存在虚假和欺诈信息, 另外一个让投资者担心的问题是资金滥用[20]。

众筹的法律监管包括以下三个方面[90]:

(1) 众筹的立法和融资者相关信息的披露标准。众筹是一种民主的投资行为[91], 必然带来管理权分散, 这对初创企业有益还是有弊[92]?

(2) 众筹环境下财务度量方式以及工具面临的挑战。资本资产定价模型(CAPM)是财务指标的基础, 在此基础上的资本加权平均成本(WACC)是被广泛接受的投资准则[93], 该理论基于风险比较计算投资回报率。但是, 众筹投资者的动机不只是投资回报率, 还包括非金钱价值和心理回报, 这很难以传统的财务指标度量。

(3) 从立法机构以及政府监管的角度上, 如何保证来自全球的投资者参与一个项目的复杂关系以及合法性?由此带来的税收问题和监管问题也亟待解决。

总体而言, 现有研究对众筹的探讨还缺乏系统性以及有影响力的研究成果。针对理论研究的不足, 进行如下的研究评述。

现有研究较多采用可直接量化的指标, 但是对那些不能直接量化的指标缺少深入探索。例如: 融资者对项目的文字介绍是一种典型的UGC, 是投资者决策的重要参考。文本描述信息对产品销量有重要影响[94], 包括语言风格[53]、文本情感[95]、主客观性[96]、欺诈 性[59]等。另外, 为了吸引投资, 融资者可以采取多种手段说服投资者。有两种不同的观点:

(1) 注重商业创意, 对商业创意进行描述和包装;

(2) 强调融资者(创业团队)的能力, 例如: 姓名、简历、专业素质、已经取得的成就等。由于时间和资源的有限性, 类似于电梯测试(Elevator Pitch), 突出了某一方面势必会削弱另外一方面, 这两种偏向性本质上是“人力资本”与“非人力资本”之间的选择, 这是未来研究的一个方向。

相对其他融资方式来说, 众筹这种融资方式是一种容易获得的资金[1], 而且众筹融资也是极具效率的一种融资方式[97], 但是容易获得的资金并不意味着就是好的资金。尤其是股权众筹, 通过众筹创建的企业是否会影响后续融资?众筹企业的IPO是否会受到分散股权的影响?众筹企业的信息披露对象应该是谁?如何保证众筹企业保密性等, 这方面的讨论还没有深入开展。众筹资金的劣势主要体现在以下三个方面:

(1) 通过设置不同的投资门槛限制了投资者的选择[98];

(2) 众筹资金的来源是广大的在线投资者, 众多投资者的参与必然导致后期的项目管理问题[99];

(3) 由于互联网信息披露要求的弱化和不规范, 投资者更可能面临欺诈; 并且开放的投资人群体抗风险能力往往更差[100]。而且, 现有研究鲜有讨论众筹的外部效应, 例如众筹融资对于产业的发展。

传统的市场交易存在本地偏好, 交易双方的地理位置会趋同。然而, 众筹项目的信息展示以及投资行为都是在线完成的, 理论上, 众筹平台打破了空间局限, 本地偏好理应不显著。但是少数研究仍然证实了本地偏好在众筹投资中存在并发挥作用, 但现有地理位置研究只涉及音乐行业[24]。音乐行业具有特殊性, 其他行业并未验证。地理位置效应是否普遍存在?地理位置效应是否依赖于社会关系?地理位置效应从投资行为角度为众筹项目研究和实践提供了新视角。

很多投资者会重复投资多个项目, 前一个项目的实施进展和对承诺的兑现程度会影响到下一次参与投资的意愿, 目前还缺少这种反馈型投资行为的研究。作为新生的金融模式, 诸多功能有待提升。例如, 适合众筹项目的个性化推荐是完善众筹模式的途径之 一[101]。反馈型研究可以完善众筹功能, 为众筹模式服务更多的初创企业和创业者提供机会。

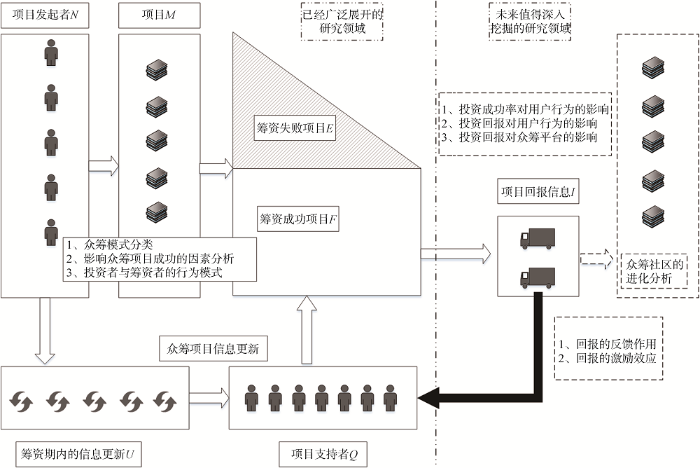

图5归纳了众筹模式的研究范畴, 现有研究主要关注图5的左半部, 对右半部较少涉及, 对于社区进化、激励、反馈等的研究还没有完全展开。

本文对基于Web的众筹模式进行综述, 重点对众筹的定义、模式、影响因素、行为模式、研究不足等方面进行梳理和总结。首先回顾了众筹的定义, 并归纳了众筹的6种实现模式: 基于回报的众筹、基于无偿捐赠的众筹、基于股权的众筹、基于借贷关系的众筹、科研众筹以及公众科学众筹。在此基础上, 对6种众筹模式的影响因素进行总结。融资成功的影响因素是众筹研究的焦点, 为此从以下几个方面展开分析: 众筹平台因素、项目描述因素、社会关系因素、地理位置因素以及项目质量因素。然后, 对融资者与投资者的行为模式进行探讨, 并对涉及的法律支持研究进行评述, 最后对已有研究进行了归纳和评述。本研究存在一些不足: 从数据来源上看, 英文数据主要来自Web of Science, 但是Web of Science中有很多来自中国的期刊和文章, 本文并未对这部分数据进行区分, 这是未来的研究内容之一。无论在理论层面还是实践

层面, 众筹模式都还有较大的可探索空间。未来的研究可着眼于多个领域与互联网金融结合, 同时推进众筹模式的行业监管和质量控制。

王伟: 提出研究思路, 设计研究方案, 论文撰写, 文献整理;

郭丽环: 论文修订, 文献收集和整理;

王洪伟: 论文框架设计, 论文最终版本修订;

Kevin Zhu: 论文总体协调, 未来研究方向梳理;

何翎: 论文修订, 文献收集和整理。

所有作者声明不存在利益冲突关系。

| [1] |

How Should Crowdfunding Research Evolve? A Survey of the Entrepreneurship Theory and Practice Editorial Board [J].https://doi.org/10.1111/etap.2017.41.issue-2 URL [本文引用: 2] |

| [2] |

A Conceptualized Investment Model of Crowdfunding [J].https://doi.org/10.1080/13691066.2013.847614 URL [本文引用: 4] 摘要

Crowdfunding is growing in popularity as a new form of both investment opportunity and source of venture capital. This article takes a view on whether crowdfunding is a replacement or an addition to traditional seed capital sources in the early stages of a new venture. With access to angel investment decreasing since the financial crisis of 2008, crowdfunding is of great importance to start-ups seeking starting capital. However, little effort has been made to define the investment model of crowdfunding with both crowdfunder and crowdfundee in mind. Drawing on an in-depth review of current literature on crowdfunding, this article creates an investment model of crowdfunding with various reward models available to investor and investee in mind. This article provides an extensive survey of the environment of crowdfunding based on current literature. It offers a jumping off point and a thorough literature review for researchers of crowdfunding, providing a detailed examination of the current landscape of crowdfunding based on available literary sources.

|

| [3] |

Understanding the Determinants of Funders’ Investment Intentions on Crowdfunding Platforms: A Trust-based Perspective [J]. |

| [4] |

The Economics of Crowdfunding Platforms [J].https://doi.org/10.1016/j.infoecopol.2015.08.003 URL [本文引用: 1] |

| [5] |

What Problems does Crowdfunding Solve? [J].https://doi.org/10.1525/cmr.2016.58.2.20 URL [本文引用: 1] 摘要

Abstract The expansion of crowdfunding raises two related questions: what type of platform suits each project and how should existing platforms expand? The answer lies in analyzing the field of crowdfunding as a solution to four specific problems: gatekeeping, coordination, inexperience, and patronage. Using an inductive analysis of the largest U.S. sites, this article identifies the range of problems crowdfunding addresses and their performance to date. Crowd funding succeeds in raising money within and across networks, but efforts to use crowdfunding to educate or to generate recurring revenue are less successful.

|

| [6] |

Emerging Technologies and the Democratisation of Financial Services: A Metatriangulation of Crowdfunding Research [J].https://doi.org/10.1016/j.infoandorg.2016.09.001 URL [本文引用: 1] |

| [7] |

Crowdfunding: Tapping the Right Crowd [J].https://doi.org/10.2139/ssrn.1578175 URL [本文引用: 3] 摘要

The basic idea of crowdfunding is to raise external finance from a large audience (the “crowd”), where each individual provides a very small amount, instead of soliciting a small group of sophisticated investors. The paper develops a model that associates crowdfunding with pre-ordering and price discrimination, and studies the conditions under which crowdfunding is preferred to traditional forms of external funding. Compared to traditional funding, crowdfunding has the advantage of offering an enhanced experience to some consumers and, thereby, of allowing the entrepreneur to practice menu pricing and extract a larger share of the consumer surplus; the disadvantage is that the entrepreneur is constrained in his/her choice of prices by the amount of capital that he/she needs to raise: the larger this amount, the more prices have to be twisted so as to attract a large number of “crowdfunders” who pre-order, and the less profitable the menu pricing scheme.

|

| [8] |

Expand Innovation Finance via Crowdfunding [J].https://doi.org/10.1126/science.aaf6989 URL PMID: 28008025 [本文引用: 1] 摘要

Downloaded from http://science.sciencemag.org/ on December 24, 2016 INSIGHTS P OLICY FORUM ENTREPRENEURIAL ECONOMICS Expand innovation finance via crowdfunding By Olav Sorenson, 1 Valentina Assenova, 1 Guan-Cheng Li, 2 Jason Boada, 2 Lee Fleming 2,3 C rowdfunding (CF) platforms, such as Kickstarter (KS), offer a means of funding innovation, connecting inven- tors and entrepreneurs with a multi- tude of supporters, who each provide a small fraction of the amount required to fund the project. Although considerable funding for innovation has historically come from venture capitalists (VCs), the entrepre- neurs funded by VCs often mirror the inves- tors in terms of their educational, social, and professional characteristics and end up con- centrated in a small number of regions (1 4). Policy-makers have thus hailed CF platforms, hoping that they will expand access to entre- preneurial finance, including among women and minority innovators, and that the inno- vations funded will create jobs and spur eco- nomic growth (5). But if particular regions, or certain sorts of individuals, routinely pro- duce better ideas (6), and VC concentrates on them, then CF might simply compete with professional investors to fund the same ideas. We find, however, that CF has been funding innovators in a large number of places that have typically been excluded from VC, and has also been expanding the geographic reach of VC itself. We compare data from 2009 to 2015 on KS campaigns and on VC investments [see supplementary materials (SM) for details on all data and analyses]. One of the dif- sciencemag.org SCIENCE 23 DECEMBER 2016 VOL 354 ISSUE 6319 Published by AAAS ILLUSTRATION: DAVIDE BONAZZI/@SALZMANART Crowdfunding attracts venture capital to new regions

|

| [9] |

McAdam R. A Rewarding Experience? Exploring How Crowdfunding is Affecting Music Industry Business Models [J].https://doi.org/10.1016/j.jbusres.2016.07.009 URL [本文引用: 1] 摘要

This paper provides an exploratory study of how rewards-based crowdfunding affects business model development for music industry artists, labels and live sector companies. The empirical methodology incorporated a qualitative, semi-structured, three-stage interview design with fifty seven senior executives from industry crowdfunding platforms and three stakeholder groups. The results and analysis cover new research ground and provide conceptual models to develop theoretical foundations for further research in this field. The findings indicate that the financial model benefits of crowdfunding for independent artists are dependent on fan base demographic variables relating to age group and genre due to sustained apprehension from younger audiences. Furthermore, major labels are now considering a more user-centric financial model as an innovation strategy, and the impact of crowdfunding on their marketing model may already be initiating its development in terms of creativity, strength and artist relations.

|

| [10] |

股权众筹助推大众创业万众创新 [J].

新常态下促进经济增长的传统动力已经减弱,中央政府希望以大众创 业、万众创新的方式找到国内经济增长的新动力.股权众筹是解决大众创业资本、资源问题的创新方式,但是定位不准确、投资不积极、委托代理等问题制约了股权 众筹的发展,本文分析了这些问题的成因,并提出了解决对策,希望能够通过股权众筹的发展促进大众创业、万众创新的政策落实.

Equity Crowdfunding to Boost the Innovation of the Public [J].

新常态下促进经济增长的传统动力已经减弱,中央政府希望以大众创 业、万众创新的方式找到国内经济增长的新动力.股权众筹是解决大众创业资本、资源问题的创新方式,但是定位不准确、投资不积极、委托代理等问题制约了股权 众筹的发展,本文分析了这些问题的成因,并提出了解决对策,希望能够通过股权众筹的发展促进大众创业、万众创新的政策落实.

|

| [11] |

Archetypes of Crowdfunding Platforms: A Multidimensional Comparison [M]. |

| [12] |

Does the Possibility to Make Equity Investments in Crowdfunding Projects Crowd out Reward-based Investments? [J].https://doi.org/10.1111/etap.2015.39.issue-1 URL [本文引用: 1] |

| [13] |

The Dynamics of Crowdfunding: An Exploratory Study [J].https://doi.org/10.2139/ssrn.2088298 URL [本文引用: 9] 摘要

Crowdfunding allows founders of for-profit, artistic, and cultural ventures to fund their efforts by drawing on relatively small contributions from a relatively

|

| [14] |

社交网络、投资者关注与股价同步性 [J].https://doi.org/10.3969/j.issn.1007-9807.2017.02.006 URL [本文引用: 1] 摘要

随着以微博、微信为代表的社交网络信息平台在中国的崛起,形成了新媒体时代下信息资讯生成与扩散的完整传播链条,深刻地影响着金融市场参与主体的学习认知习惯、投资决策理念、交易行为模式,最终影响不同金融资产的价格波动规律.本文在新媒体时代情景下,以社交网络信息披露与传播平台为切入点,基于信息关注度、信赖度、更新频率等三层维度,构建社交网络微博信息质量指标体系,研究社交网络信息质量与股价同步性的内在关联关系.研究表明:微博信息质量与股价同步性有着显著的高度负向线性关联性,并且呈现出非线性U型关系.即随着社交网络信息质量水平的提升,股价同步性逐渐降低到达最小值,而后又逐渐提高.研究结论为证明上市公司社交网络微博平台对股价同步性有较强影响力,提供了中国金融市场的证据.

Social Networks, Investor Attention and Stock Price Synchronicity [J].https://doi.org/10.3969/j.issn.1007-9807.2017.02.006 URL [本文引用: 1] 摘要

随着以微博、微信为代表的社交网络信息平台在中国的崛起,形成了新媒体时代下信息资讯生成与扩散的完整传播链条,深刻地影响着金融市场参与主体的学习认知习惯、投资决策理念、交易行为模式,最终影响不同金融资产的价格波动规律.本文在新媒体时代情景下,以社交网络信息披露与传播平台为切入点,基于信息关注度、信赖度、更新频率等三层维度,构建社交网络微博信息质量指标体系,研究社交网络信息质量与股价同步性的内在关联关系.研究表明:微博信息质量与股价同步性有着显著的高度负向线性关联性,并且呈现出非线性U型关系.即随着社交网络信息质量水平的提升,股价同步性逐渐降低到达最小值,而后又逐渐提高.研究结论为证明上市公司社交网络微博平台对股价同步性有较强影响力,提供了中国金融市场的证据.

|

| [15] |

Crowdfunding Creative Ideas: The Dynamics of Project Backers in Kickstarter [J].https://doi.org/10.2139/ssrn.2234765 URL [本文引用: 6] 摘要

Entrepreneurs are turning to crowdfunding as a way to finance their creative ideas. Crowdfunding involves relatively small contributions of many consumer-inves

|

| [16] |

The Influence of Online Information on Investing Decisions of Reward-based Crowdfunding [J].https://doi.org/10.1016/j.jbusres.2016.10.001 URL [本文引用: 2] 摘要

61This study is one of the first to introduce the elaboration likelihood model to the crowdfunding literature.61Compare two routes (the central route and the peripheral route), which have higher influence on the funders’ investment decisions.61Examine the role of electronic word of mouth in the crowdfunding context.61Demonstrate that project or product type has an important moderating impact on the correlation between online information and funder investment decisions.

|

| [17] |

Is Crowdfunding Different? Evidence on the Relation Between Gender and Funding Success from a German Peer-to-Peer Lending Platform [J]. |

| [18] |

Show me the Money!: An Analysis of Project Updates During Crowdfunding Campaigns [C]// |

| [19] |

基于发起人视角的创意众筹异质性激励机制研究 [J].The Heterogeneous Incentive Mechanism of Creative Crowdfunding Based on the Perspective of Entrepreneurs [J]. |

| [20] |

Crowdfunding:Motivations and Deterrents for Participation [J]. |

| [21] |

竞争环境下众筹产品的定价策略研究 [J].https://doi.org/10.13587/j.cnki.jieem.2017.04.027 URL [本文引用: 1] 摘要

拥有想法却无法从传统渠道筹集资金的微创企业,可以通过在众筹网站发布众筹项目获取投资。然而,由于我国知识产权保护方面的法律尚不完善、申请专利时间长流程繁琐等原因,公开发布产品信息存在信息泄露的风险,拥有资金的其他企业可能模仿其创意生产类似的产品。本文研究这类模仿所带来的竞争对众筹企业在各阶段(众筹阶段与销售阶段)最优定价的影响。本文研究的主要思路是:通过建立各阶段的利润目标函数,得出相应的最优利润与定价策略,分析相关参数对各企业总利润与定价的影响,并以传统的银行融资模式为标杆,比较分析众筹融资下企业决策行为的变化。最后,本文将模型拓展到模仿具有成本的情况,进一步分析了此时众筹企业的决策行为和模仿企业的质量决策,探讨了模仿成本内生对企业决策行为的影响。

Pricing Strategy of Crowdfunding Products in Competitive Environment [J].https://doi.org/10.13587/j.cnki.jieem.2017.04.027 URL [本文引用: 1] 摘要

拥有想法却无法从传统渠道筹集资金的微创企业,可以通过在众筹网站发布众筹项目获取投资。然而,由于我国知识产权保护方面的法律尚不完善、申请专利时间长流程繁琐等原因,公开发布产品信息存在信息泄露的风险,拥有资金的其他企业可能模仿其创意生产类似的产品。本文研究这类模仿所带来的竞争对众筹企业在各阶段(众筹阶段与销售阶段)最优定价的影响。本文研究的主要思路是:通过建立各阶段的利润目标函数,得出相应的最优利润与定价策略,分析相关参数对各企业总利润与定价的影响,并以传统的银行融资模式为标杆,比较分析众筹融资下企业决策行为的变化。最后,本文将模型拓展到模仿具有成本的情况,进一步分析了此时众筹企业的决策行为和模仿企业的质量决策,探讨了模仿成本内生对企业决策行为的影响。

|

| [22] |

Determinants of Backers’ Funding Intention in Crowdfunding: Social Exchange Theory and Regulatory Focus [J].https://doi.org/10.1016/j.tele.2016.06.006 URL [本文引用: 1] |

| [23] |

基于复制动态的消费者众筹策略演化动态 [J].https://doi.org/10.12011/1000-6788(2017)11-2812-09 URL [本文引用: 2] 摘要

采用大群体反复博弈.复制动态演化博弈,在公平贡献和利他主义两种情景下,建立了有限理性的消费者群体通过模仿学习不断调整支持众筹和不支持众筹两策略多人博弈的演化系统.通过对不同参数变化对系统演化稳定均衡及吸引域的影响分析,研究了存在消费者后悔度条件下各因素对众筹演化成功的影响机制.研究发现,公平贡献机制下不考虑后悔度,则支持众筹策略占优,考虑众筹失败带给消费者后悔产生负效益时,当融资目标越小,产品质量越高,消费者偏好越大,团体效用越大,越有利于众筹演化成功,然而发行份额的增加会带给消费者搭便车的投机行为,从而抑制众筹成功.在利他主义策略下,消费者偏好、产品质量和团体效用越大,越有利于众筹演化成功,但是当融资目标不变而发行份额增加时,消费者搭便车的行为却没有增加,反而提高了众筹演化成功的概率.

Evolutionary Dynamics of Consumers’ Crowdfunding Strategies Based on Replicator Dynamics [J].https://doi.org/10.12011/1000-6788(2017)11-2812-09 URL [本文引用: 2] 摘要

采用大群体反复博弈.复制动态演化博弈,在公平贡献和利他主义两种情景下,建立了有限理性的消费者群体通过模仿学习不断调整支持众筹和不支持众筹两策略多人博弈的演化系统.通过对不同参数变化对系统演化稳定均衡及吸引域的影响分析,研究了存在消费者后悔度条件下各因素对众筹演化成功的影响机制.研究发现,公平贡献机制下不考虑后悔度,则支持众筹策略占优,考虑众筹失败带给消费者后悔产生负效益时,当融资目标越小,产品质量越高,消费者偏好越大,团体效用越大,越有利于众筹演化成功,然而发行份额的增加会带给消费者搭便车的投机行为,从而抑制众筹成功.在利他主义策略下,消费者偏好、产品质量和团体效用越大,越有利于众筹演化成功,但是当融资目标不变而发行份额增加时,消费者搭便车的行为却没有增加,反而提高了众筹演化成功的概率.

|

| [24] |

Crowdfunding: Geography, Social Networks, and the Timing of Investment Decisions [J].https://doi.org/10.1111/jems.12093 URL [本文引用: 5] 摘要

Abstract Top of page Abstract 1.Introduction 2.Empirical Setting 3.Empirical Strategy 4.Results 5.Conclusion References Supporting Information We examine a crowdfunding platform that connects artists with funders. Although the Internet reduces many distance-related frictions, local and distant funders exhibit different funding patterns. Local funders appear less responsive to information about the cumulative funds raised by an artist. However, this distance effect appears to proxy for a social effect: it is largely explained by funders who likely have an offline social relationship with the artist (“friends and family”). Yet, this social effect does not persist past the first investment, suggesting that it may be driven by an activity like search but not monitoring. Thus, although the platform seems to diminish many distance-sensitive costs, it does not eliminate all of them. These findings provide a deeper understanding of the abilities and limitations of online markets to facilitate transactions and convey information between buyers and sellers with varying degrees of social connectedness.

|

| [25] |

Appealing to the Crowd: Ethical Justifications in Canadian Medical Crowdfunding Campaigns [J].https://doi.org/10.1136/medethics-2016-103933 URL PMID: 28137998 [本文引用: 1] 摘要

ABSTRACTMedical crowdfunding is growing in terms of the number of active campaigns, amount of funding raised andpublic visibility. Little is known about how campaigners appeal to potential donors outside of anecdotal evidence collected in news reports on specific medicalcrowdfunding campaigns. This paper offers a first steptowards addressing this knowledge gap by examiningmedical crowdfunding campaigns for Canadianrecipients. Using 80 medical crowdfunding campaignsfor Canadian recipients, we analyse how Canadiansjustify to others that they ought to contribute to funding their health needs. We find the justificationscampaigners tend to fall into three themes: personalconnections, depth of need and giving back. We further discuss how these appeals can understood in terms ofethical justifications for giving and how thesejustifications should be assessed in light of the academic literature on ethical concerns raised by medicalcrowdfunding.

|

| [26] |

什么样的评论更容易获得有用性投票——以亚马逊网站研究为例 [J].

【目的】购物网站评论系统中的投票机制有利于帮助消费者筛选出高质量评论。本文以评论有用性投票数为研究对象,探讨什么样的评论更容易获得有用性投票。【方法】以信息采纳理论和负面偏差理论为基础,基于亚马逊购物网站中的12 393条手机评论数据,结合文本分析与零膨胀负二项回归分析方法,从评论者信度、评论信息质量、评论极性三个方面探究评论有用性投票影响因素。【结果】研究结果表明,评论者有用性、评论信息量、评论回复数、极端评分、评论文本消极倾向对评论有用性投票数具有积极正向影响。评论者发表评论数、评论者是否确认购买对评论有用性投票数有负向影响。【局限】仅以手机这一搜索型产品为研究对象,研究结果欠缺普适性。【结论】本文研究成果对于改善电子商务评论排序系统具有借鉴意义。

Identifying Reviews with More Positive Votes—Case Study of Amazon.cn [J].

【目的】购物网站评论系统中的投票机制有利于帮助消费者筛选出高质量评论。本文以评论有用性投票数为研究对象,探讨什么样的评论更容易获得有用性投票。【方法】以信息采纳理论和负面偏差理论为基础,基于亚马逊购物网站中的12 393条手机评论数据,结合文本分析与零膨胀负二项回归分析方法,从评论者信度、评论信息质量、评论极性三个方面探究评论有用性投票影响因素。【结果】研究结果表明,评论者有用性、评论信息量、评论回复数、极端评分、评论文本消极倾向对评论有用性投票数具有积极正向影响。评论者发表评论数、评论者是否确认购买对评论有用性投票数有负向影响。【局限】仅以手机这一搜索型产品为研究对象,研究结果欠缺普适性。【结论】本文研究成果对于改善电子商务评论排序系统具有借鉴意义。

|

| [27] |

Effects of the Price of Charitable Giving: Evidence from an Online Crowdfunding Platform [J].https://doi.org/10.1016/j.jebo.2014.04.010 URL [本文引用: 3] 摘要

A long literature has examined the effects of the price of giving – that is, the amount an individual must give for one dollar to accrue to the charitable activity itself – on donative behavior. We use data from DonorsChoose.org, an online platform linking teachers with prospective donors that are uniquely suited to addressing this question due to exogenous variation in overhead costs. An increased price of giving results in a lower likelihood of a project being funded. We also calculate the price elasticity of giving, finding estimates between 610.8 and 612. Finally, we examine the effect of competition on giving and find that increased competition reduces the likelihood of a project being funded. These results provide insight into the workings of the market for charitable gifts.

|

| [28] |

The Social Network Effect: The Determinants of Giving Through Social Media [J].https://doi.org/10.1177/0899764013485159 URL [本文引用: 1] |

| [29] |

The Value of Completing Crowdfunding Projects [C]// |

| [30] |

Peer Effects in Charitable Giving: Evidence from the (Running) Field [J].https://doi.org/10.1111/ecoj.12114 URL [本文引用: 1] 摘要

There is a widespread belief that peer effects are important in charitable giving but little evidence on how donors respond to their peers. Analysing a unique data set of donations to online fund‐raising pages, we find positive and sizeable peer effects: a 0510 increase in the mean of past donations increases giving by 052.50, on average. Donations respond to both very large and very small amounts and to changes in the mode. We find little evidence that donations signal charity quality – our preferred explanation is that donors use information on earlier donations to decide what is appropriate for them to give.

|

| [31] |

Non-profit Differentials in Crowd-based Financing: Evidence from 50,000 Campaigns [J].https://doi.org/10.1016/j.econlet.2014.03.022 URL [本文引用: 1] 摘要

61We assess empirically if non-profit crowdfunding projects are unusually successful.61Within our database, we classify more than 2000 projects as non-profits.61They receive higher average pledges and are more likely to reach their funding goals.61Yet, they also obtain lower total funding amounts and have fewer funding providers.61A small number of very successful for-profit projects is important for the results.

|

| [32] |

股权众筹投资者动机研究 [J].https://doi.org/10.19571/j.cnki.1000-2995.2017.12.009 URL [本文引用: 1] 摘要

基于自我决定理论,构建了以内在动机为解释变量,外在动机为调节变量,投资意愿为被解释变量的股权众筹投资者动机模型。运用探索性因子分析和二分类Logit模型对560位股权众筹投资者的问卷调查数据进行实证检验,研究发现:(1)助人动机和信任动机荷载于一个共同因子,命名为基于信任的助人动机;(2)内在动机中基于信任的助人动机、社交动机对股权众筹投资意愿有正向影响,而支持动机的作用不显著;(3)外在动机中获取奖励的动机对股权众筹投资意愿有负向影响,而经济收益动机的作用不显著;(4)外在动机中的经济收益动机和获取奖励动机均对基于信任的助人动机与投资意愿之间、社交动机与投资意愿之间有显著的正向调节作用。

A Study of the Investor Motivation of Equity Crowdfunding [J].https://doi.org/10.19571/j.cnki.1000-2995.2017.12.009 URL [本文引用: 1] 摘要

基于自我决定理论,构建了以内在动机为解释变量,外在动机为调节变量,投资意愿为被解释变量的股权众筹投资者动机模型。运用探索性因子分析和二分类Logit模型对560位股权众筹投资者的问卷调查数据进行实证检验,研究发现:(1)助人动机和信任动机荷载于一个共同因子,命名为基于信任的助人动机;(2)内在动机中基于信任的助人动机、社交动机对股权众筹投资意愿有正向影响,而支持动机的作用不显著;(3)外在动机中获取奖励的动机对股权众筹投资意愿有负向影响,而经济收益动机的作用不显著;(4)外在动机中的经济收益动机和获取奖励动机均对基于信任的助人动机与投资意愿之间、社交动机与投资意愿之间有显著的正向调节作用。

|

| [33] |

Some Simple Economics of Crowdfunding [J].https://doi.org/10.1086/674021 URL [本文引用: 1] 摘要

It is not surprising that the financing of early-stage creative projects and ventures is typically geographically localized since these types of funding decisions are usually predicated on personal relationships and due diligence requiring face-to-face interactions in response to high levels of risk, uncertainty, and information asymmetry. So, to economists, the recent rise of crowdfunding—raising capital from many people through an online platform—which offers little opportunity for careful due diligence and involves not only friends and family but also many strangers from near and far, is initially startling. On the eve of launching equity-based crowdfunding, a new market for early-stage finance in the United States, we provide a preliminary exploration of its underlying economics. We highlight the extent to which economic theory, in particular transaction costs, reputation, and market design, can explain the rise of nonequity crowdfunding and offer a framework for speculating on how equity-based crowdfunding may unfold. We conclude by articulating open questions related to how crowdfunding may affect social welfare and the rate and direction of innovation.

|

| [34] |

Predictors of Capital Structure in Small Ventures [J].

What are the key determinants of capital structure of small ventures? We empirically examined the question by analyzing capital structure decisions of 903 small ventures. Six categories of predictors were included in the analysis: goal orientation of the entrepreneur, business outlook for the enterprise, stock of human capital input, strategic changes made, gender, and life-stage of the enterprise. Goal orientation, especially satisfaction with economic need, and odds of success of the firm are among the most important predictors of equity vs. debt and internal equity vs. external equity financing. The results suggest that entrepreneurs' personal characteristics play a key role in capital structure decisions.

|

| [35] |

Why Research on Women Entrepreneurs Needs New Directions [J].https://doi.org/10.1111/j.1540-6520.2006.00138.x URL [本文引用: 1] 摘要

Research articles on women's entrepreneurship reveal, in spite of intentions to the contrary and in spite of inconclusive research results, a tendency to recreate the idea of women as being secondary to men and of women's businesses being of less significance or, at best, as being a complement. Based on a discourse analysis, this article discusses what research practices cause these results. It suggests new research directions that do not reproduce women's subordination but capture more and richer aspects of women's entrepreneurship.

|

| [36] |

Strategic Herding Behavior in Peer-to-Peer Loan Auctions [J].https://doi.org/10.1016/j.intmar.2010.07.001 URL [本文引用: 1] 摘要

Online Peer-to-Peer (P2P) loan auctions enable individual consumers to borrow and lend money directly to one another. We study herding behavior, defined as a greater likelihood of bidding in auctions with more existing bids, in P2P loan auctions on Prosper.com. The results of an empirical study provide evidence of to the point at which it has received full funding. After this point, herding diminishes (a 1% increase in bids increases the likelihood of an additional bid by only 5%). We also find a positive association between herding in the loan auction and its subsequent performance, that is, whether borrowers pay the money back on time. Unlike eBay auctions where herding impacts bidders adversely, our findings reveal that strategic herding behavior in P2P loan auctions benefits bidders, individually and collectively.

|

| [37] |

Rational Herding in Microloan Markets [J].https://doi.org/10.1287/mnsc.1110.1459 URL [本文引用: 4] 摘要

Microloan markets allow individual borrowers to raise funding from multiple individual lenders. We use a unique panel data set that tracks the funding dynamics of borrower listings on Prosper.com, the largest microloan market in the United States. We find evidence of rational herding among lenders. Well-funded borrower listings tend to attract more funding after we control for unobserved listing heterogeneity and payoff externalities. Moreover, instead of passively mimicking their peers (irrational herding), lenders engage in active observational learning (rational herding); they infer the creditworthiness of borrowers by observing peer lending decisions and use publicly observable borrower characteristics to moderate their inferences. Counterintuitively, obvious defects (e.g., poor credit grades) amplify a listing's herding momentum, as lenders infer superior creditworthiness to justify the herd. Similarly, favorable borrower characteristics (e.g., friend endorsements) weaken the herding effect, as lenders attribute herding to these observable merits. Follow-up analysis shows that rational herding beats irrational herding in predicting loan performance.

|

| [38] |

Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending [J].https://doi.org/10.1287/mnsc.1120.1560 URL [本文引用: 1] |

| [39] |

Competition Between Microfinance NGOs: Evidence from Kiva [J].https://doi.org/10.1016/j.worlddev.2011.09.009 URL [本文引用: 1] 摘要

This paper investigates empirically the effect of competition between microfinance NGOs seeking subsidized capital from individual social investors. Although NGO behavior in competitive environments is often subject to controversy, there is little formal empirical evidence to illustrate theoretical findings and inform policy. Using data from Kiva, an online peer-to-peer (P2P) microfinance platform, we find that competition has a sizable negative impact on projects funding speed and that the effect is stronger between close substitutes. This is important because competition for subsidized capital implies organizational pressures similar to those faced when NGOs compete for donations.

|

| [40] |

Cultural Differences and Geography as Determinants of Online Pro-social Lending [J].https://doi.org/10.2139/ssrn.2271298 URL [本文引用: 2] 摘要

In this paper, we analyze patterns of transaction between individuals using data drawn from Kiva.org, a global online crowdfunding platform that facilitates prosocial, peer-to-peer lending. Our analysis, which employs an aggregate dataset of country-to-country lending volumes based on more than three million individual lending transactions that took place between 2005 and 2010, considers the dual roles of geographic distance and cultural differences on lenders0964 decisions about which borrowers to support. While cultural differences have seen extensive study in the Information Systems literature as sources of friction in extended interactions, here, we argue and demonstrate their role in individuals0964 selection of a transaction partner. We present evidence that lenders do prefer culturally similar and geographically proximate borrowers. An analysis of the marginal effects indicates that an increase of one standard deviation in the cultural differences between lender and borrower countries is associated with 30 fewer lending actions, while an increase of one standard deviation in physical distance is associated with 0.23 fewer lending actions. We also identify a substitution effect between cultural differences and physical distance, such that a 50 percent increase in physical distance is associated with an approximate 30 percent decline in the effect of cultural differences. Considering approaches to overcoming the observed cultural effect, we offer some empirical evidence of the potential of IT-based trust mechanisms, focusing on Kiva0964s reputation rating system for microfinance intermediaries. We discuss the implications of our findings for prosocial lending, online crowdfunding, and electronic markets more broadly.

|

| [41] |

第三方电子交易平台的双边市场特征——基于在线个人借贷市场的实证分析 [J].https://doi.org/10.3969/j.issn.1007-9807.2016.01.005 URL [本文引用: 1] 摘要

以Prosper在线个人借贷平台为研究对象,实证考察了第三方电子交易市场中用户的交叉网络外部性、自网络外部性和平台定价策略对双边用户效用和平台利润的影响.结果表明:受市场供小于求、平台运营模式和借贷双方交易行为的影响,新借入者规模对借出者收入、前期借出者总规模对借入者需求均产生了显著的正交叉网络外部性;借入者之间由于竞争存在负自网络外部性,而借出者之间由于协同关系存在正自网络外部性;借贷双方对平台交易费具有显著的负价格弹性,平台利润与借贷双方的交易费分别呈现二次线性关系;在市场供小于求的情况下,平台利润主要受到借出者规模及其费率的影响.

Two-sided Characteristics of the Third-party Electronic Market: Evidence from Online Peer-to-Peer Lending Marketplace [J].https://doi.org/10.3969/j.issn.1007-9807.2016.01.005 URL [本文引用: 1] 摘要

以Prosper在线个人借贷平台为研究对象,实证考察了第三方电子交易市场中用户的交叉网络外部性、自网络外部性和平台定价策略对双边用户效用和平台利润的影响.结果表明:受市场供小于求、平台运营模式和借贷双方交易行为的影响,新借入者规模对借出者收入、前期借出者总规模对借入者需求均产生了显著的正交叉网络外部性;借入者之间由于竞争存在负自网络外部性,而借出者之间由于协同关系存在正自网络外部性;借贷双方对平台交易费具有显著的负价格弹性,平台利润与借贷双方的交易费分别呈现二次线性关系;在市场供小于求的情况下,平台利润主要受到借出者规模及其费率的影响.

|

| [42] |

Learning by Doing with Asymmetric Information: Evidence from Prosper. com[R] . |

| [43] |

利用众筹模式拓宽科研经费的筹集渠道 [J].Expanding the Channels of Research Funds Raising Through Crowdfunding [J]. |

| [44] |

科技类奖励众筹支持者参与动机及参与意愿影响因素研究 [J].

以奖励众筹中科技类项目为研究对象,分析支持者心理动机及其支持行为的影响因素。提出了支持者的三重角色(消费者、投资者和社会人),以及发起人能力和从众两个影响因素。通过结构方程进行验证,结论为:科技类众筹项目支持者具备消费者动机(独特性产品需求)和投资者动机(投机心理),但是不具备社会人动机(亲社会倾向)。发起人能力对支持者支持众筹项目有正向影响;从众因素方面,模仿行为对支持者支持众筹项目有正向影响,而自我心理折扣的影响则不显著。

Motivation and Influence Factors of Funders Supporting the Technology Reward Crowdfunding Project [J].

以奖励众筹中科技类项目为研究对象,分析支持者心理动机及其支持行为的影响因素。提出了支持者的三重角色(消费者、投资者和社会人),以及发起人能力和从众两个影响因素。通过结构方程进行验证,结论为:科技类众筹项目支持者具备消费者动机(独特性产品需求)和投资者动机(投机心理),但是不具备社会人动机(亲社会倾向)。发起人能力对支持者支持众筹项目有正向影响;从众因素方面,模仿行为对支持者支持众筹项目有正向影响,而自我心理折扣的影响则不显著。

|

| [45] |

Raising Money for Scientific Research Through Crowdfunding [J]. |

| [46] |

Funding from the Crowd: An Internet-based Crowdfunding Platform to Support Business Set-ups from Universities [J].https://doi.org/10.1142/S0218843013400078 URL [本文引用: 1] |

| [47] |

Crowd Science: The Organization of Scientific Research in Open Collaborative Projects [J].https://doi.org/10.1016/j.respol.2013.07.005 URL [本文引用: 2] |

| [48] |

创新项目大众筹资:资助人公民行为的价值 [J].

互联网与民间资本的结合产生了大众筹资模式(简称众筹),资助人不仅在众筹网站为创新项目提供资金,而且主动辅助项目的执行。如何利用资助人的公民行为提高项目实施绩效是一个重要的学术问题。本文基于价值共创、价值与满意度方面理论,采用问卷调查法研究资助人公民行为对满意度的作用,以及公民行为的影响因素。主要有三点贡献:1首次从价值共创角度分析众筹项目的执行过程;2揭示了资助人公民行为、社区收益与满意度的关系;3验证了感知的项目风险、项目新颖度、社会责任感对资助人公民行为的影响。

The Crowdfunding of Innovation Projects: The Value of Sponsors’ Citizenship Behaviors [J].

互联网与民间资本的结合产生了大众筹资模式(简称众筹),资助人不仅在众筹网站为创新项目提供资金,而且主动辅助项目的执行。如何利用资助人的公民行为提高项目实施绩效是一个重要的学术问题。本文基于价值共创、价值与满意度方面理论,采用问卷调查法研究资助人公民行为对满意度的作用,以及公民行为的影响因素。主要有三点贡献:1首次从价值共创角度分析众筹项目的执行过程;2揭示了资助人公民行为、社区收益与满意度的关系;3验证了感知的项目风险、项目新颖度、社会责任感对资助人公民行为的影响。

|

| [49] |

Galaxy Zoo: Morphologies Derived from Visual Inspection of Galaxies from the Sloan Digital Sky Survey [J].https://doi.org/10.1111/mnr.2008.389.issue-3 URL [本文引用: 1] |

| [50] |

Next Steps for Citizen Science [J].https://doi.org/10.1126/science.1251554 URL [本文引用: 1] |

| [51] |

Crowdfunding in Europe: Determinants of Platform Creation Across Countries [J].https://doi.org/10.1525/cmr.2016.58.2.44 URL [本文引用: 1] 摘要

Abstract While the crowdfunding phenomenon has attracted considerable practitioner and scholarly attention, existing research predominantly reflects a U.S.-centric perspective. This article examines crowdfunding platform creation in 15 European countries. Despite the omnipresent reach of the internet, national boundaries shape the evolution of the European crowdfunding industry. Specifically, crowdfunding platform creation varies across countries and distinct national patterns emerge for crowdfunding activity in general. Moreover, econometric analyses suggest that country-level factors influence platform creation in European countries, with interesting variations across four crowdfunding models: Donation, Reward, Lending, and Equity.

|

| [52] |

基于用户间信任关系改进的协同过滤推荐方法 [J].Improving Collaborative Filtering Recommendation Based on Trust Relationship Among Users [J]. |

| [53] |

众筹融资成功率与语言风格的说服性——基于Kickstarter的实证研究 [J].

众筹融资效果决定着众筹平台的兴衰。众筹行为很大程度上是由投资者的主观因素决定的,而影响主观判断的一个重要因素就是语言的说服性。而这又是一种典型的用户产生内容(UGC),项目发起者可以采用任意类型的语言风格对项目进行描述。不同的语言风格会改变投资者对项目前景的感知,进而影响他们的投资意愿。首先,依据Aristotle修辞三元组以及Hovland说服模型,采用扎根理论,将众筹项目的语言说服风格分为5类:诉诸可信、诉诸情感、诉诸逻辑、诉诸回报和诉诸夸张。然后,借助文本挖掘方法,构建说服风格语料库,并对项目摘要进行分类。最后,建立语言说服风格对项目筹资影响的计量模型,并对Kickstarter平台上的128345个项目进行实证分析。总体来说,由于项目性质的差异,不同的项目类别对应于不同的最佳说服风格。

The Success Rate of Crowdfunding and the Persuasiveness of Language Style — An Empirical Study Based on Kickstarter [J].

众筹融资效果决定着众筹平台的兴衰。众筹行为很大程度上是由投资者的主观因素决定的,而影响主观判断的一个重要因素就是语言的说服性。而这又是一种典型的用户产生内容(UGC),项目发起者可以采用任意类型的语言风格对项目进行描述。不同的语言风格会改变投资者对项目前景的感知,进而影响他们的投资意愿。首先,依据Aristotle修辞三元组以及Hovland说服模型,采用扎根理论,将众筹项目的语言说服风格分为5类:诉诸可信、诉诸情感、诉诸逻辑、诉诸回报和诉诸夸张。然后,借助文本挖掘方法,构建说服风格语料库,并对项目摘要进行分类。最后,建立语言说服风格对项目筹资影响的计量模型,并对Kickstarter平台上的128345个项目进行实证分析。总体来说,由于项目性质的差异,不同的项目类别对应于不同的最佳说服风格。

|

| [54] |

Education and Income Inequality: New Evidence from Cross-country Data [J].https://doi.org/10.1111/1475-4991.00060 URL [本文引用: 1] 摘要

Abstract This paper presents empirical evidence on how education is related to income distribution in a panel data set covering a broad range of countries for the period between 1960 and 1990. The findings indicate that educational factors—higher educational attainment and more equal distribution of education —play a significant role in making income distribution more equal. The results also confirm the Kuznets inverted–U curve for the relationship between income level and income inequality. We also find that government social expenditure contributes to more equal distribution of income. However, a significant proportion of cross–country variation in income inequality remains unexplained.

|

| [55] |

The Determinants of Default on Insured Conventional Residential Mortgage Loans [J].https://doi.org/10.2307/2327587 URL [本文引用: 1] 摘要

This paper presents empirical evidence on the determinants of default for insured residential mortgages. A multinomial logit model is specified and estimated for regional aggregates constructed from cross sectional and time series data. The results document the independent statistical significance of contemporaneous payment/income and loan/value ratios and unemployment rates as well as more commonly studied determinants of default such as age and the original loan/value ratio.

|

| [56] |

基于任务展示示能性的众筹项目视频分析——以众筹网为例 [J].Analyzing Crowdfunding Videos Based on Task Presentation — Case Study of zhongchou.com [J]. |

| [57] |

The Psychological Meaning of Words: LIWC and Computerized Text Analysis Methods [J].https://doi.org/10.1177/0261927X09351676 URL [本文引用: 2] |

| [58] |

Entrepreneur Passion and Preparedness in Business Plan Presentations: A Persuasion Analysis of Venture Capitalists’ Funding Decisions [J].https://doi.org/10.5465/amj.2009.36462018 URL [本文引用: 1] |

| [59] |

A Comparison of Classification Methods for Predicting Deception in Computer-mediated Communication [J].https://doi.org/10.1080/07421222.2004.11045779 URL [本文引用: 2] |

| [60] |

Persuasion in Fundraising Letters: An Interdisciplinary Study [J].https://doi.org/10.1177/0899764009339216 URL [本文引用: 1] 摘要

In this paper, we report experimental evidence on the effectiveness of several techniques of persuasion commonly utilized in direct-mail solicitation. The study is built on theory-based, descriptive models of fundraising discourse and on comparisons of recommended and actual practices related to three dimensions of persuasion: rhetorical, visual, and linguistic. The specific rhetorical variable included is persuasive appeal (rational, credibility, or affective). The visual variable selected for the study is the presence or absence of bulleted lists, and the linguistic variable included is readability, or the complexity of exposition. Subjects were presented with pairs of fictive direct-mail appeals from imaginary universities that differ in these dimensions and asked to allocate a hypothetical $100 across each pair. Results suggest that letters utilizing credibility appeals and letters written at a high level of readability produce the highest donations.

|

| [61] |

Valuation of Crowdfunding: Benefits and Drawbacks [J].https://doi.org/10.5755/j01.em.18.1.3713 URL [本文引用: 1] 摘要

The aim of this paper is to broaden the body of knowledge about crowdfunding.Crowdfunding is an innovative and relatively new concept that connects investors to entrepreneurs. It is a method of fundraising, based on the ability to pool money from individuals in order to turn promising ideas into actual businesses.02Crowdfunding is presently growing very fast and this growth will probably be magnified after the anticipated changes in law are made.02Due to the novelty of the approach, a number of problems and fears arises, what might lead to an underestimation of the approach and possibly missed opportunities.02Taking a look at crowdfunding through the prism of the SWOT analysis allows obtaining a comprehensive picture of the subject. The strengths of crowdfunding are: a chance to test marketability, the accessibility of capital, benefits for communities, rights to make company’s decisions stay in the hands of entrepreneurs. Weaknesses include administrative and accounting challenges, the possibility of ideas being stolen, weaker investor protection and potential for fraud, also, crowdfunding is exceptionally internet based, so investors might lack advice. Identified opportunities include the existence of niche, information society and positive effects crowdfunding is expected to have on economy, also, such threats as the risky nature of small business and unsuitable legal restrictions arise.02Gaining deeper understanding about crowdfunding could be useful for entrepreneurs choosing a way to raise capital and investors seeking for different investment opportunities.

|

| [62] |

Success Factors of Crowdfunding Projects on the Kickstarter Platform [M]. |

| [63] |

Social Identity and Signalling Success Factors in Online Crowdfunding [J].https://doi.org/10.1080/08985626.2016.1198425 URL [本文引用: 2] 摘要

Online crowdfunding means relying on the Internet to seek financial support from the general public. In this paper we examine success factors in the social capital networks of the top 5000 most funded projects in Kickstarter.com at the time of this study. We first look at how fundraisers and backers identify themselves with the projects they support in their own social networks. This is modelled using Facebook friends, and Facebook shares, respectively, guided by social identity theory. Secondly, we use signalling theory to investigate crowdfunding success based on backers and fundraisers ability to engage in a forum, modelled using the number of comments between them, or with unilateral signals using the number of updates from the fundraiser. This study suggests that funders and backers who identify themselves with the projects in their own social networks are associated with greater pledge/backer ratio. We also find that projects where the fundraiser and its backers exchange more signals in a joint forum, but not signals delivered unilaterally by the fundraiser, have a greater pledge/backer ratio. These findings, based on a scalable quantitative study, highlight the importance of a multi-theory approach, advance social identity theory and signalling theory in the context of crowdfunding, and could be applied to online and normal entrepreneurship environments alike.

|

| [64] |

从众还是旁观?众筹市场中出资者行为的实证研究 [J].https://doi.org/10.13587/j.cnki.jieem.2016.04.016 URL [本文引用: 2] 摘要

了解众筹市场中的出资者行为是提高众筹项目成功率的前提。潜在出资者面对已有筹资信息可能表现出两种截然不同的行为:羊群的从众行为和责任扩散的旁观行为。为了探讨众筹过程中已有筹资信息对潜在出资者决策的影响,本文基于羊群行为理论和责任扩散理论,以Demohour中393个众筹项目的面板数据为研究样本,分析了潜在出资者的行为模式。研究结果表明,潜在出资者行为会受到责任扩散效应影响,并且该效应会在已有经验型出资较多时或达到目标筹资额后得到强化,但面对目标筹资额相对较高的项目时,潜在出资者会因责任扩散效应弱化而提高出资额。同时,研究还发现捐赠类和回报类项目出资者均表现为责任扩散的旁观行为,但是其决策行为受到不同变量的调节效应。

Herding or Bystander? An Empirical Study of the Backers’ Behavior in Crowdfunding Market [J].https://doi.org/10.13587/j.cnki.jieem.2016.04.016 URL [本文引用: 2] 摘要

了解众筹市场中的出资者行为是提高众筹项目成功率的前提。潜在出资者面对已有筹资信息可能表现出两种截然不同的行为:羊群的从众行为和责任扩散的旁观行为。为了探讨众筹过程中已有筹资信息对潜在出资者决策的影响,本文基于羊群行为理论和责任扩散理论,以Demohour中393个众筹项目的面板数据为研究样本,分析了潜在出资者的行为模式。研究结果表明,潜在出资者行为会受到责任扩散效应影响,并且该效应会在已有经验型出资较多时或达到目标筹资额后得到强化,但面对目标筹资额相对较高的项目时,潜在出资者会因责任扩散效应弱化而提高出资额。同时,研究还发现捐赠类和回报类项目出资者均表现为责任扩散的旁观行为,但是其决策行为受到不同变量的调节效应。

|

| [65] |

Understanding the Importance of Interaction Between Creators and Backers in Crowdfunding Success [J].https://doi.org/10.1016/j.elerap.2017.12.004 URL [本文引用: 1] |

| [66] |

Venture Capital and Private Equity Contracting: An International Perspective [M]. |

| [67] |

Success Factors in Title III Equity Crowdfunding in the United States [J].https://doi.org/10.1016/j.elerap.2017.12.001 URL [本文引用: 2] 摘要

Title III of the JOBS Act took effect in May 2016 and it began a new chapter in equity crowdfunding in the United States by providing an opportunity for entrepreneurial ventures to solicit funding from non-accredited investors. Due to the relative novelty, little is known about factors that can affect equity crowdfunding success under Title III. To address this gap in research, we draw on the risk capital framework and we examine the effects of market, execution and agency risks in equity crowdfunding under Title III. We collect data on 133 ventures that attracted more than $11 million in funding commitments across sixteen Title III equity crowdfunding platforms. We find that all three types of risks can affect the likelihood of successful fundraising under Title III. We discuss the implications of these findings for entrepreneurs, investors, crowdfunding platforms and policy makers.

|

| [68] |

Does My Contribution to Your Crowdfunding Project Matter? [J].https://doi.org/10.1016/j.jbusvent.2016.10.004 URL [本文引用: 1] 摘要

61People want to help others if they believe that their contribution really matters.61Crowdfunding support increases as a project approaches its target goal.61Crowdfunding support decreases once the target goal is reached.61There are several moderators of this goal gradient effect.

|

| [69] |

Investment Behavior Prediction in Heterogeneous Information Network [J].https://doi.org/10.1016/j.neucom.2015.12.139 URL [本文引用: 1] 摘要

The crowdfunding industry is growing rapidly worldwide and poses new challenges on how to understand investment behavior. Indeed, a key challenge in this area is how to measure the similarity of an investor and a company, or the interest of an investor in a company. Tremendous effort has been made in previous research regarding the single effective factor or homogeneous network model based on link prediction for investment behavior prediction. In this study, we build an investment behavior prediction model of meta-path-based heterogeneous network, which considers multiple entity and relation types associated with the investment behavior of a particular investor. Our investment behavior prediction model provides an effective similarity measure function for meta-path. To validate the proposed model, we perform experiments on real-world data from CrunchBase. Experimental results reveal that our investment behavior prediction model is indeed a useful indicator.

|

| [70] |

Home Bias in Online Investments: An Empirical Study of an Online Crowdfunding Market [J].https://doi.org/10.2139/ssrn.2219546 URL [本文引用: 1] 摘要

An extensive literature in economics and finance has documented home bias , the tendency that transactions are more likely to occur between parties in the same geographical area rather than outside. Using data from a large online crowdfunding marketplace and employing a quasi-experimental design, we find evidence that home bias still exists in this virtual marketplace for financial products. Furthermore, through a series of empirical tests, we show that rationality-based explanations cannot fully explain such behavior and that behavioral reasons at least partially drive this remarkable phenomenon. As crowdfunding becomes an alternative and increasingly appealing channel for financing, a better understanding of home bias in this new context provides important managerial, practical, and policy implications. This paper was accepted by Lee Fleming, entrepreneurship and innovation .

|

| [71] |

Is the Crowd Sensitive to Distance?— How Investment Decisions Differ by Investor Type [J].https://doi.org/10.1007/s11187-016-9834-6 URL [本文引用: 1] 摘要

Abstract This paper presents the first evidence of the influence of geographic distance among retail, accredited, and overseas investors and venture location in an equity crowdfunding context. By analyzing investment decisions, we show that geographic distance is negatively correlated with investment probability for all home country investors. Our comparison of home country and overseas investors reveals that overseas investors are not sensitive to distance. However, when comparing only home country investors (subdivided into retail and accredited), we document that both investor types are similarly sensitive to the distance of possible ventures.

|

| [72] |

The Economics of Entrepreneurship [M]. |

| [73] |

Angel Finance: The Other Venture Capital [J].https://doi.org/10.2139/ssrn.941228 URL [本文引用: 1] 摘要

Angel financing is one of the most common, but least studied methods, to finance new ventures. In this paper, I propose a model to explain angel behavior. I use

|

| [74] |

Show Me the Right Stuff: Signals for High-Tech Startups [J].https://doi.org/10.1111/jems.12012 URL [本文引用: 1] 摘要

We present a theoretical model of startup signaling with multiple signals and potential differences in external investor preferences. For a novel sample of technology incubator startups, we empirically examine the use of patents and founder, friends, and family (FFF) money as such signals, finding that they are jointly endogenous to venture capital and business angel investment in the startups. For this sample, venture capitalists appear to value patents more highly than FFF money, while the reverse is true for business angels. Moreover, the impact of patents on venture capitalists is larger than the impact of FFF money on business angels.

|

| [75] |

融资者个人因素以及社会关系对食品类众筹项目的影响研究 [J].The Impact of Personal Factors and Social Relationships of the Financers on the Food-related Crowdfunding Campaigns [J]. |

| [76] |

Should Investors Bet on the Jockey or the Horse? Evidence from the Evolution of Firms from Early Business Plans to Public Companies [J].https://doi.org/10.1111/j.1540-6261.2008.01429.x URL [本文引用: 1] |

| [77] |

Why We Plan: The Impact of Nascent Entrepreneurs’ Cognitive Characteristics and Human Capital on Business Planning [J].https://doi.org/10.1002/sej.1197 URL [本文引用: 1] |

| [78] |

Funders’ Positive Affective Reactions to Entrepreneurs’ Crowdfunding Pitches: The Influence of Perceived Product Creativity and Entrepreneurial Passion [J].https://doi.org/10.1016/j.jbusvent.2016.10.006 URL [本文引用: 1] |

| [79] |

The Barriers Facing Artists’ Use of Crowdfunding Platforms: Personality, Emotional Labor, and Going to the Well One Too Many Times [J]. |

| [80] |

Equity Retention and Social Network Theory in Equity Crowdfunding [J].https://doi.org/10.1007/s11187-016-9710-4 URL [本文引用: 1] 摘要

After comparing the regulation and development of equity crowdfunding around the world, this paper investigates the signaling role played toward crowdfunders by

|

| [81] |

Managing the Risks of Equity Crowdfunding: Lessons from China [J].https://doi.org/10.1080/14735970.2017.1296217 URL [本文引用: 1] 摘要

The Chinese experience shows that equity crowdfunding platforms fail to perform their role as neutral intermediaries in the distribution of information relating

|

| [82] |

Start-up Absorptive Capacity: Does the Owner’s Human and Social Capital Matter? [J].https://doi.org/10.1177/0266242612475103 URL [本文引用: 1] |

| [83] |

Serial Crowdfunding, Social Capital Project Success [J].https://doi.org/10.1111/etap.12271 URL [本文引用: 1] 摘要

In this paper, we focus attention on serial crowdfunders, that is, entrepreneurs who repeatedly turn to crowdfunding to finance their projects. We argue that serial crowdfunders take advantage of the social contacts with those that backed their previous campaigns. This internal social capital developed within the platform, which is not available to “normal” serial entrepreneurs, makes serial crowdfunders' campaigns more successful than those launched by novice crowdfunders. However, this type of social capital is a substitute for the internal social capital built by backing other campaigns, and has a limited lifespan. Econometric results on a sample of 31,389 Kickstarter campaigns confirm our contentions. Implications for research, practice, and policy are discussed.

|

| [84] |

Entrepreneurial Implications of Crowdfunding as Alternative Funding Source for Innovations [J].https://doi.org/10.1080/13691066.2015.1037132 URL [本文引用: 1] 摘要

Crowdfunding (CF) is a form of early-stage financing for innovative ventures, which has seen tremendous growth in the past few years – partly because it provides a desperately needed alternative to the scarcity of traditional sources of finance during the so called ‘credit crunch’. CF ranges from a simple form of pre-financing to full grown debt or equity investments, but they are typically small pledges that can add up to incredible amounts. Scholarly literature has only started to examine CF and is still in an early stage when it comes to identifying implications for entrepreneurs apart from often over-simplified anecdotal evidence of success. The authors argue that CF can by no means be seen from a financial perspective only, rather it needs to be addressed as a bundle of processes leading to innovative entrepreneurial business-models. This qualitative study explores four extreme cases from the information and communications technology sphere to find out non-financial implications of CF as alternative funding source for innovative entrepreneurs and their business models.

|

| [85] |

我国众筹成功影响因素及羊群现象研究 [J].https://doi.org/10.13956/j.ss.1001-8409.2016.02.02 URL [本文引用: 1] 摘要

搜集众筹项目样本和融资过程中的数据,对驱动众筹项目成功的因素和众筹市场的羊群现象进行了实证研究和行为金融实验检验。实证研究发现,众筹项目的关注人数、互动话题数、价格梯度、筹资周期对众筹项目成功有显著正向影响,众筹社会媒介数量对筹资绩效没有显著影响,筹资周期与实际筹资额呈倒U型关系,众筹项目筹资绩效不存在显著的性别差异和组织类型差异。众筹项目在筹资过程中存在羊群现象,众筹投资羊群行为实验证实了这一现象。

Successful Factors and Herding Phenomenon of Crowdfunding [J].https://doi.org/10.13956/j.ss.1001-8409.2016.02.02 URL [本文引用: 1] 摘要

搜集众筹项目样本和融资过程中的数据,对驱动众筹项目成功的因素和众筹市场的羊群现象进行了实证研究和行为金融实验检验。实证研究发现,众筹项目的关注人数、互动话题数、价格梯度、筹资周期对众筹项目成功有显著正向影响,众筹社会媒介数量对筹资绩效没有显著影响,筹资周期与实际筹资额呈倒U型关系,众筹项目筹资绩效不存在显著的性别差异和组织类型差异。众筹项目在筹资过程中存在羊群现象,众筹投资羊群行为实验证实了这一现象。

|

| [86] |

Crowdsourcing New Product Ideas Under Consumer Learning [J].https://doi.org/10.2139/ssrn.1974211 URL [本文引用: 1] 摘要

We propose a dynamic structural model that illuminates the economic mechanisms shaping individual behavior and outcomes on crowdsourced ideation platforms. We

|

| [87] |

McKelvey B. The Wisdom of Crowds in the Movie Industry: Towards New Solutions to Reduce Uncertainties [J]. |

| [88] |

The Backer-Developer Connection: Exploring Crowdfunding’s Influence on Video Game Production [J]. |

| [89] |

Risk Aversion and Wealth: Evidence from Person-to-Person Lending Portfolios [J].https://doi.org/10.2139/ssrn.1507902 URL [本文引用: 1] 摘要

We estimate risk aversion from the actual financial decisions of 2,168 investors in Lending Club (LC), a person-to-person lending platform. We develop a methodology that allows us to estimate risk aversion parameters from each portfolio choice. Since the same individual makes repeated investments, we are able to construct a panel of risk aversion parameters that we use to disentangle heterogeneity in attitudes towards risk from the elasticity of investor-specific risk aversion to changes in wealth. In the cross section, we find that wealthier investors are more risk averse. Using changes in house prices as a source of variation, we find that investors become more risk averse after a negative wealth shock. These preferences consistently extrapolate to other investor decisions within LC.

|

| [90] |

Crowdfunding Social Ventures: A Model and Research Agenda [J].https://doi.org/10.1080/13691066.2013.782624 URL [本文引用: 2] 摘要

Crowdfunding (CF) in a social entrepreneurship (SE) context is praised in media narrations for its multifaceted potential. From an academic point of view, little has been written about CF as a whole, and enquiries from the SE sphere are mostly concerned with donation-based CF. This paper first reviews extant literature on financing social ventures and CF. Based upon the findings, the author draws up a schema of CF's inner workings and subsequently discusses it in an SE context. From this model, a research agenda consisting of eight themes is derived: types and utility functions; corporate governance; investor relations, reporting and risk; opportunity recognition; networking; legitimacy; financial metrics and legal and regulatory hurdles.

|

| [91] |

Democratizing Innovation and Capital Access: The Role of Crowdfunding [J].https://doi.org/10.1525/cmr.2016.58.2.72 URL [本文引用: 1] 摘要

Abstract This article focuses on how crowdfunding might democratize the commercialization of innovation as well as financing. First, it examines how crowdfunders decide what effort to support and asks how do crowd and expert decisions differ? Second, it investigates whether crowdfunding democratizes access to capital by asking whether groups that have historically been underrepresented in capital markets gain additional access to capital markets through crowdfunding. Finally, it investigates whether crowdfunding leads to the growth of new firms in the same way that traditional funding does. Taken together, these questions point at a potentially vast alternative infrastructure for developing, funding, and commercializing innovation.

|

| [92] |

Kicking Off Social Entrepreneurship: How a Sustainability Orientation Influences Crowdfunding Success [J].https://doi.org/10.1111/joms.2016.53.issue-5 URL [本文引用: 1] |

| [93] |

On the Cost of Capital in Inventory Models with Deterministic Demand [J].https://doi.org/10.1016/j.ijpe.2016.10.007 URL [本文引用: 1] 摘要

In the operations management literature, the financial risk in an inventory model is usually assumed to be captured by the (constant) weighted average cost of capital (WACC) of the firm. This assumption is, at best, an approximation, since this cost depends on the risk of the cash flows, which, in turn, depends on the inventory policy. We investigate what the right cost of capital should be in an inventory model with deterministic demand. To do so, we study an inventory model with a generic inventory cost function where risk depends on the inventory decision made. Additive and multiplicative financial noise functions are included to assess the impact of these on both the cost of capital of the firm and the optimal inventory policy. We find that, in contrast to previous models, risk is not in general a monotone function of inventory. Also, a rate close to the risk-free rate, which typically deviates significantly from the WACC, should be used to value inventory-related investments when the inventory cost function is dominated by holding cost for large order quantities, even if investments are subject to other sources of financial variability.

|

| [94] |

基于情感及影响力的微博用户群体特征分析——以A手机为例 [J].Analyzing Characteristics of Weibo Users Based on Their Sentiments and Influences — Case Study of Cell Phone Brand [J]. |

| [95] |

评论文本对酒店满意度的影响:基于情感分析的方法 [J].The Impacts of Reviews on Hotel Satisfaction:A Sentiment Analysis Method [J]. |

| [96] |

The Determinants of Crowdfunding Success: A Semantic Text Analytics Approach [J].https://doi.org/10.1016/j.dss.2016.08.001 URL [本文引用: 1] 摘要

In the era of the Social Web, crowdfunding has become an increasingly more important channel for entrepreneurs to raise funds from the crowd to support their startup projects. Previous studies examined various factors such as project goals, project durations, and categories of projects that might influence the outcomes of the fund raising campaigns. However, textual information of projects has rarely been studied for analyzing crowdfunding successes. The main contribution of our research work is the design of a novel text analytics-based framework that can extract latent semantics from the textual descriptions of projects to predict the fund raising outcomes of these projects. More specifically, we develop the Domain-Constraint Latent Dirichlet Allocation (DC-LDA) topic model for effective extraction of topical features from texts. Based on two real-world crowdfunding datasets, our experimental results reveal that the proposed framework outperforms a classical LDA-based method in predicting fund raising success by an average of 11% in terms of F 1 score. The managerial implication of our research is that entrepreneurs can apply the proposed methodology to identify the most influential topical features embedded in project descriptions, and hence to better promote their projects and improving the chance of raising sufficient funds for their projects.

|

| [97] |

关于众筹模式及其效率和问题 [J].

众筹模式是近年来随着互联网的发展而兴起的新型项目融资模式。众筹模式经过几年的探索实践,可以说已经取得了阶段性的成功。通过研究发现,作为一个融资方式来讲,众筹模式是有效率的。众筹之所以受到追捧是因为除了融资效率,众筹还能为创业公司带来市场、人才等紧缺资源。

On the Model of Crowdfunding and Its Efficiency and Problems [J].

众筹模式是近年来随着互联网的发展而兴起的新型项目融资模式。众筹模式经过几年的探索实践,可以说已经取得了阶段性的成功。通过研究发现,作为一个融资方式来讲,众筹模式是有效率的。众筹之所以受到追捧是因为除了融资效率,众筹还能为创业公司带来市场、人才等紧缺资源。

|

| [98] |

The Benefits of Online Crowdfunding for Fund-seeking Business Ventures [J].https://doi.org/10.1002/jsc.1955 URL [本文引用: 1] 摘要

Crowdfunding through the Internet, a new fundraising technique for small business ventures, can benefit fund-seeking companies by helping to overcome funding difficulties, providing value-added involvement, facilitating access to further funding, providing publicity and contacts, and enabling fundraising with only limited or no loss of control and ownership.

|

| [99] |

股权众筹支持创业企业融资问题研究 [J].A Study on Equity-based Crowdfunding to Support Venture Enterprises Financing [J]. |

| [100] |

股权众筹是否真的那么美——基于美国制度缺陷的再思考 [J].https://doi.org/10.13262/j.bjsshkxy.bjshkx.161206 URL [本文引用: 1] 摘要

股权众筹作为初创企业采用的一种利用互联网向大众募集小额资本的融资方式,以"脱媒式"对接投融资双方的优势,利用互联网的人群聚集与信息广泛传播效应,降低投融资方之间沟通成本,有助于投融资意向的快速达成。2012年美国JOBS法案的高调出台,吸引了全球范围内的广泛关注。但股权众筹制度在美国已受到诸多批判,除信息披露要求弱化引发的欺诈风险增加外,在注重前端融资效率的同时却忽略了投资端的设计和保护,尤其是众筹股权的流通和退出问题等。美国立法与实践领域对于这些问题尚未取得彻底的突破。股权众筹以美国模式为样板引入中国,在遭遇中国固有法律体系及制度的困扰后,中国股权众筹实践陷入更多困境。通过对美国相关制度出台的背景及存在的不足进行分析,对照中国实践,锁定实践中产生的新问题,并深入探讨现有解决路径能否真正缓解这些不足,以期对股权众筹制度重新进行明确的定位。

Is Equity Crowdfunding Really So Agreeable? ——Rethinking Based on Defects of the US Mechanism [J].https://doi.org/10.13262/j.bjsshkxy.bjshkx.161206 URL [本文引用: 1] 摘要

股权众筹作为初创企业采用的一种利用互联网向大众募集小额资本的融资方式,以"脱媒式"对接投融资双方的优势,利用互联网的人群聚集与信息广泛传播效应,降低投融资方之间沟通成本,有助于投融资意向的快速达成。2012年美国JOBS法案的高调出台,吸引了全球范围内的广泛关注。但股权众筹制度在美国已受到诸多批判,除信息披露要求弱化引发的欺诈风险增加外,在注重前端融资效率的同时却忽略了投资端的设计和保护,尤其是众筹股权的流通和退出问题等。美国立法与实践领域对于这些问题尚未取得彻底的突破。股权众筹以美国模式为样板引入中国,在遭遇中国固有法律体系及制度的困扰后,中国股权众筹实践陷入更多困境。通过对美国相关制度出台的背景及存在的不足进行分析,对照中国实践,锁定实践中产生的新问题,并深入探讨现有解决路径能否真正缓解这些不足,以期对股权众筹制度重新进行明确的定位。

|

| [101] |

众筹项目的个性化推荐:面向稀疏数据的二分图模型 [J].https://doi.org/10.12011/1000-6788(2017)04-1011-13 URL [本文引用: 1] 摘要

二分图模型是一种全局优化算法,本文将二分图模型应用于直接推荐众筹项目,使用Per—sonalRank算法迭代计算网络节点的全局关联度,从而推荐那些基于余弦相似度的协同过滤不能有效推荐的项目,适用性更加广泛.更进一步,提出将二分图模型与协同过滤算法相结合,首先把网络结构划分为二分图,采用二分图算法得到的两类节点(用户节点,项目节点)之间的全局相似度,再结合协同过滤算法,得到基于二分图模型的协同过滤算法.实验表明,在众筹项目推荐中,由于数据极端稀疏,适宜采用二分图模型来进行相似度计算并进行推荐.

Personalized Recommendation of Crowd-funding Campaigns: A Bipartite Graph Approach for Sparse Data [J].https://doi.org/10.12011/1000-6788(2017)04-1011-13 URL [本文引用: 1] 摘要

二分图模型是一种全局优化算法,本文将二分图模型应用于直接推荐众筹项目,使用Per—sonalRank算法迭代计算网络节点的全局关联度,从而推荐那些基于余弦相似度的协同过滤不能有效推荐的项目,适用性更加广泛.更进一步,提出将二分图模型与协同过滤算法相结合,首先把网络结构划分为二分图,采用二分图算法得到的两类节点(用户节点,项目节点)之间的全局相似度,再结合协同过滤算法,得到基于二分图模型的协同过滤算法.实验表明,在众筹项目推荐中,由于数据极端稀疏,适宜采用二分图模型来进行相似度计算并进行推荐.

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}